The below video from Bloomberg highlights the going thesis on the Street as to why the price of lumber has been falling, namely that it is an issue of oversupply.

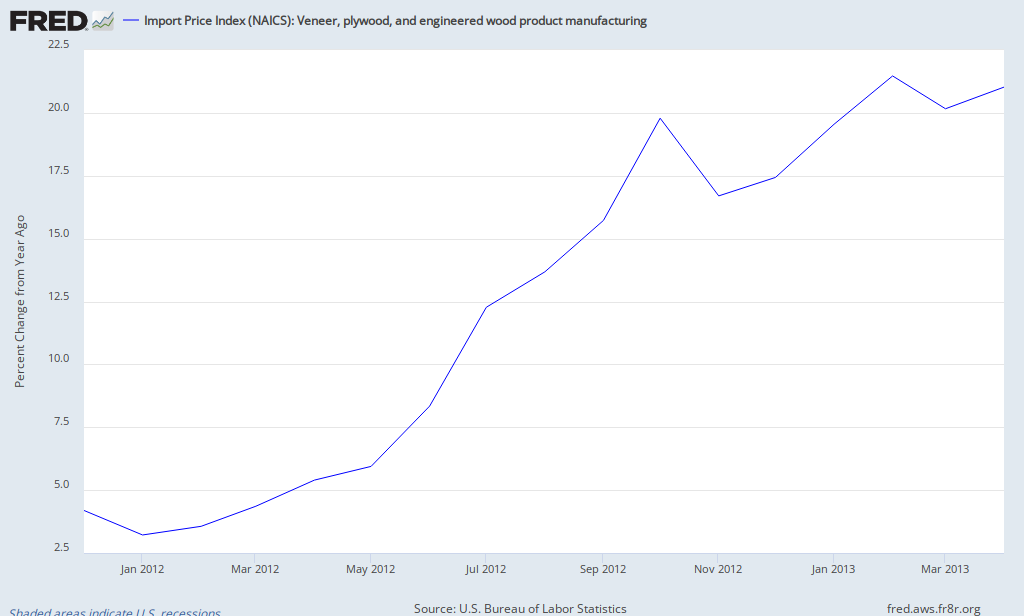

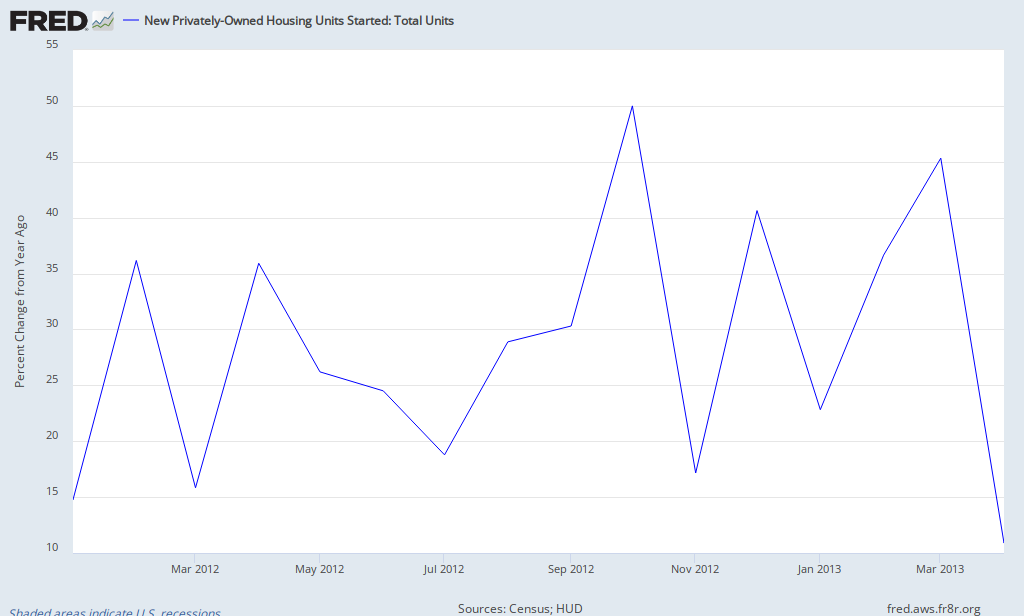

This may very well be the case and the recent decline from $400 may just be a correction. However, I think the data here is mixed. First, lets look at year-over-year lumber production

Lumber production has been increased at year-over-year rate between 17.5% and roughly 21% since the end of 2012. The acceleration in growth could be the reason for the decline in lumber prices and may lead credence into the supply-side thesis.

But, housing starts- although volatile- have been increasing at a year-over-year growth rate between 20% to 42% over the same period, ahead of the growth in lumber production. Aside from the deceleration in April, which may have spooked the market, this picture does not scream a supply issue to me, as the difference remains positively in favor of lumber.

Looking at the price and volume characteristics of the lumber future contracts, their does appear to be some volume off the high characteristics (albeit hard to discern in the below chart) in the beginning of April this year. The LB1 contract came off nears high in the early days of April on 2x to 3x the average volume. This could suggest that traders and other operators are seeing something not readily known on the Street.

This is a dynamic to watch in the coming months. In the last few days, lumber looks to have caught a bid at about the $280 support level and volume has come in. This may foreshadow a stabilization in lumber prices. It also may just be a head fake. If it is and it is just operators trying to goose prices to get out of positions, then lumber prices are heading lower.

Considering this relationship between lumber and the homebuilders (here shown as the Homebuilders Spider ETF, ticker XHB) ........

......... a further decline in lumber prices may call into question the durability of the homebuilders stock rally and the whole housing market recovery.

This may very well be the case and the recent decline from $400 may just be a correction. However, I think the data here is mixed. First, lets look at year-over-year lumber production

Lumber production has been increased at year-over-year rate between 17.5% and roughly 21% since the end of 2012. The acceleration in growth could be the reason for the decline in lumber prices and may lead credence into the supply-side thesis.

But, housing starts- although volatile- have been increasing at a year-over-year growth rate between 20% to 42% over the same period, ahead of the growth in lumber production. Aside from the deceleration in April, which may have spooked the market, this picture does not scream a supply issue to me, as the difference remains positively in favor of lumber.

Looking at the price and volume characteristics of the lumber future contracts, their does appear to be some volume off the high characteristics (albeit hard to discern in the below chart) in the beginning of April this year. The LB1 contract came off nears high in the early days of April on 2x to 3x the average volume. This could suggest that traders and other operators are seeing something not readily known on the Street.

This is a dynamic to watch in the coming months. In the last few days, lumber looks to have caught a bid at about the $280 support level and volume has come in. This may foreshadow a stabilization in lumber prices. It also may just be a head fake. If it is and it is just operators trying to goose prices to get out of positions, then lumber prices are heading lower.

Considering this relationship between lumber and the homebuilders (here shown as the Homebuilders Spider ETF, ticker XHB) ........

......... a further decline in lumber prices may call into question the durability of the homebuilders stock rally and the whole housing market recovery.

No comments:

Post a Comment