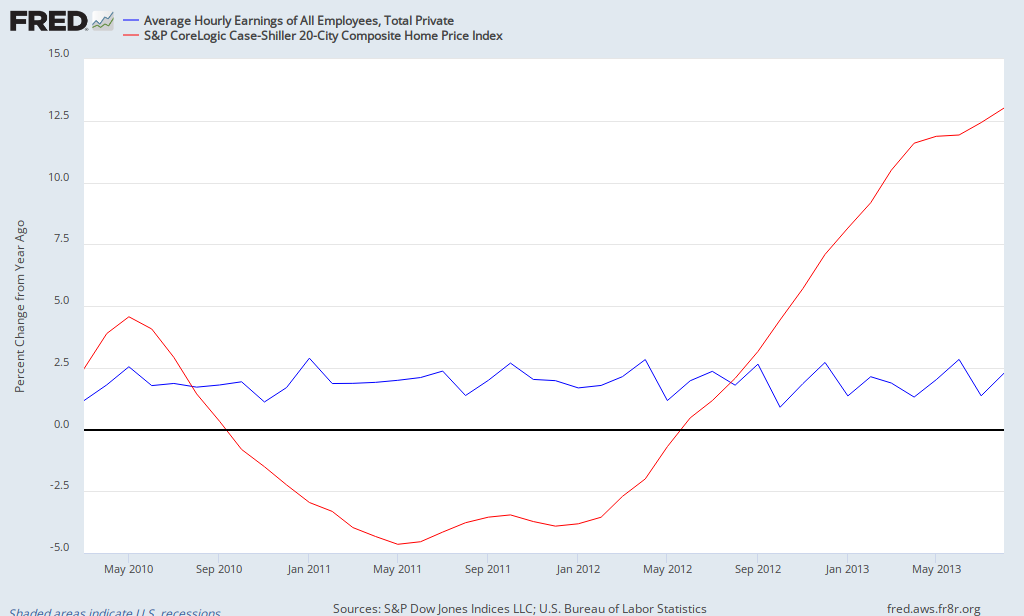

As I have been saying and showing here, the economy is far weaker than most assume or believe. Although I thought the Fed was going to taper 'their' purchases with an emphasis on the their (noting that money growth has slowed significantly, but just recently picking up), I am also not surprised the Fed did not pull back on the purchases of treasury and other debt. Following this week's events, my odds are pick'em that the Fed will pull back this year. Your guess is as good as mine.

Saturday, September 21, 2013

Friday, September 20, 2013

Illogic in Fractional Reserve Banking

by James E. Miller of the Ludwig von Mises Institue

If there was one business venture the leftist and forgotten “Occupy” movement was right to distrust, it was the banking industry. In the wake of the 2008 financial crisis and subsequent bailing out of the world’s financial system by fascist states, taxpayers – especially the progressive types – were correct to feel amiss. But rather than take a scrutinizing look into the privilege afforded to the banking class, the outraged took to political action in the callow hope of correcting a wrong.

The underlying chicanery behind fractional reserve banking has

existed since the days of Plato. Modern technology has not negated the

rationale used to discover and affirm natural law. Binary codes on a

computer screen do not create a new reality. The governing doctrines of

humanity are, in de Soto’s words, “unchanging and inherent in the logic

of human relationships.” While fractional reserve banking could exist

in a free market environment and regulate itself through vigorous

competition, that theoretical scenario does not prove the entire fulcrum

of the business rests on solid ground.

If there was one business venture the leftist and forgotten “Occupy” movement was right to distrust, it was the banking industry. In the wake of the 2008 financial crisis and subsequent bailing out of the world’s financial system by fascist states, taxpayers – especially the progressive types – were correct to feel amiss. But rather than take a scrutinizing look into the privilege afforded to the banking class, the outraged took to political action in the callow hope of correcting a wrong.

Like any popular uprising, the goal was quickly smothered

in favor of further rent-seeking. Instead of aiming consternation at the

incestuous relationship between government and the money-changers,

occupiers wanted the quick-fix of redistribution. The cries of “this is

what democracy looks like” might as well have been “this is what

panhandling looks like.” Centralized banking went unquestioned. The

nature of fractional reserve practices was ignored – or likely not

understood by the pea-brained

philosophers. Still, the radical levellers who set-up camp in Zuccotti

Park were on to something by asking why their precious public officials

voted to shore up the balance sheets of a disproportionately small

member caste.

Banking is, to put it bluntly, a strange and unique

business. The industry is centuries-old, and the legality of its

operations has been questionable since inception. I am referring

specifically to the practice of bankers lending out claimed reserves – a

contentious issue among libertarian theorists. If the larger public

were to become privy to this business model, it may spark a troubling

curiosity in the less-moneyed class. But then again, this author never

ceases to be amazed by the bounds of common apathy.

In banking, certain legal doctrines have guided the trade

since antiquity, including the nature of contracts. The violation of

these distinct forms of lawful guarantees once carried the weight of

justice. But no longer; as the deliberately obscuring practice of

loaning out deposits meant to be available on-demand has created such

instability in the banking system, the incessant teetering on the cliff

of insolvency remains an ever viable threat to economic tranquility.

Libertarians – specifically those schooled in the Austrian,

causal-realist tradition of economics – are intellectually miles ahead

of the Occupy folks when it comes to the study of currency. And while

the students of Mises and Hayek are fervently opposed to any central

bank management, there remains a sharp divide on the ethics of

fractional reserve banking. In a recent missive in the Freeman, economist Malavika Nair questions

the Rothbardian ethic that finds the practice of banks creating credit

out of thin air fraudulent. The piece, which deconstructs the dean of

the Austrian school’s original argument, frames banking away from the

supposed cut-and-dry thinking model of anti-fractionalists.

Nair begins with a false choice by asking: “Would

fractional reserve banking exist in a world without a central bank? Put

another way: Is fractional reserve banking inherently fraudulent?”

These statements are not one in the same; they reference two separate

conditions. Absent central banking, unbacked credit expansion could

still exist. Back in mid-to-late 19th century America where the Federal

Reserve was still a twinkle in the centralizers’ eyes, fractional

reserve banking and pyramiding credit were common practice. The question at hand is whether such business is based on a fraudulent understanding of the nature of goods.

Nair finds issue with the essence of contracts and how they

relate to the duty of those individuals entrusted with safeguarding

money. The contract

– an extension of humanity’s self-ownership and free will – has been a

recognized covenant enforceable by compulsion for as long as man first

conceived of himself as an autonomous being. It finds legitimacy in the

human understanding of bonds and keeping one’s word. The evolution of common law

has dictated that any activity stipulated in a compact cannot entail

unlawful activity. To enforce an illegal activity would thereby be a

crime in itself – an ipso facto contradiction in reason.

The contract is key for banking operations. Nair argues

that bank functions, both deposit and lending, are plainly justifiable;

the discrepancy arises in the manner that customer funds are utilized.

Currently, bankers freely lend out money that is available on command

by both the borrower and depositor. In practice, this is the creation

of two goods from one ex nihilo. In a totally isolated instance where a

bank were to service only two patrons, the act of creating what Mises

called “fiduciary media” would appear as the very perversion of

intuitive law it embodies. It would simply come off as no more than a

violation of the known rules of the world.

Nair counters by asserting that a “claim to money is not

the same thing as the money itself.” This is a confusing affirmation as

antagonists to fractional reserve banking hardly make that claim. The

point of contention is that promissory notes for bank deposits represent

real money, though they may circulate as mediums of exchange and

fulfill the role of currency. Should two or more of these “I owe you”

certificates be created to represent one unit of bank reserves available

on-demand, there is a direct and unquestionable inconsistency. It is

certainly true, as Nair points out, that the fungible quality of money

dictates it be treated differently than non-substitutable goods.

However, the fact that cash is interchangeable does not dismiss its

limited character.

If the principle of unbacked expansion of credit were

applied to other industries such as automobiles or condominiums, titles

to the same good could theoretically be multiplied, but not without

controversy. Having two titles for one car is not based on logic or a

firm understanding of universal law. You simply cannot create real,

definite material by declaration. Nair asserts that this is not true

when it comes to the market of money. In his words, the over-issuing of

redeemable bank notes “does not mean one thing is in two places at the

same time” but that “two different things are in two places at the same

time.” This is only so much sophistry, as the claims to bank reserves

are still representative of real goods. There may be multiple slips of

paper representing one unit of money-proper floating around in the

economy, but that does not dismiss the plain and true fact that there

are more claims than what is available.

As economist Jesús Huerta de Soto documents in his tour de force Money, Bank Credit, and Economic Cycles,

government has played a leading role in fostering this banking fraud

for centuries. The state is forever on the search for more resources to

carry out its bidding. Cooperation with the leading money-lending

institutions was an obvious route for subverting the moral means to

wealth creation. Since the days of classical Greece, it was well

understood that transactions of present goods fundamentally differed

from those involving future goods. In practical terms, deposits for

safekeeping were of considerable difference to those made for the strict

purpose of lending out and garnering a return. Bankers who

misappropriated funds were often found guilty of fraud and forced to pay

restitution. In one recorded episode, ancient Grecian legal scholar

Isocrates lambasted Athenian banker Passio for reneging on a client’s

depository claim. After being entrusted to hold a select amount of

money, the sly banker loaned out a portion of the funds in the hopes of

earning a profit. When asked to make due on the deposit, the timid

Passio pleaded to his accuser to keep the transgression “a secret so it

would not be discovered he had committed fraud.”

The truth remains, and will always remain, that an organic

product is not replicable through any kind of witch doctoring. A thing

is a thing is a thing. Any money substitute that represents a real

piece of fungible currency cannot pertain to that which is not in

existence. Such is the lawful understanding that goes back to the time

preceding the Hellenisitc period.

Malavika Nair offers an interesting argument by trying to

justify the practice of creating something out of nothing; but it

ultimately fails. The free lunch of artificial credit creation is

nothing more than slipping out of the baker’s shop without paying. It

would have served the Occupy crowd well to have recognized this shaky

foundation upon which the modern financial system rests. Perhaps their

message of widespread corruption would have been better received – at

least more so than by creating

shanty towns and defecating on the street. Instead, we were gifted with

a muddled and confused political message made by an irate minority who

hadn’t a clue of the forces that govern their own lives.

Bill Nygren Talks Investing Process and Valuation

Via Gurufocus a great deal of information in this interview.

Q: How do you identify undervalued companies? How much time does it take you to transform a checklist passer into an investment reality (i.e. from detecting the opportunity until it is in your portfolio)?

A: We compute our estimates of business value and look for companies selling at large discounts. When we value a stock, we first value the unlevered company, and then adjust for debt or cash to obtain a per-share value. Our favorite metric to base a valuation off of is the cash acquisition price of a similar company. In the absence of good comparable acquisitions we will consider as inputs acquisitions of businesses with similar characteristics from other industries, public market comparables, discounted cash flow models and so on. Our goal is to determine the maximum price an all cash buyer could pay to own the entire business and still earn an adequate return on their investment.

The time it takes can vary broadly. Sometimes an idea is so clear that within a week of starting work on it one concludes it should be purchased. Other times a stock can remain on our “research underway” list for years with no conclusion. I’ve found that our best ideas typically don’t linger very long in the “in process” stage. As Buffett says, it’s OK to decide a stock belongs in the “too tough pile.”

Q: As you've been investing for many years, your circle of competence grows and grows. What are some leading qualities of companies that finally attract you to make a purchase? Furthermore, when you analyze a company, what are some commonalities in the way you value them? For example, you may project growth for three years, then the company matures.

A: Most of our opportunities come from the very long term time horizon we use. When we model a company our analysts will do full financials two years out, then use an annual per-share value growth rate for the following five years, effectively giving us a 7 year forecast horizon. Most analysts use at most a two year horizon, and most stocks are traded based on even shorter horizons. A typical opportunity for us comes from negative news that we believe is cyclical that the market treats as if it is permanent. As an example, given weak economies today in most of Europe, current European car sales are beneath the level necessary to keep the car population flat. Many analysts are calculating business values based on static European sales, and conclude that auto businesses are appropriately valued. We don’t believe that Europe’s car population is going to go into secular decline. Therefore, we base our valuations off of sales much higher than are occurring today. As a result, we conclude that many global auto companies are cheap.

Q: What are some qualitative characteristics that you look for when buying shares in a company?

A: We look at many of the same characteristics other long term investors look at – competitive landscape, strength of brands, risk of disruption, and so on. But there are two questions that I think we pay more attention to than most investors do: Does forecasted growth require capital investment or will excess cash be generated? And how does management evaluate how to raise needed capital or invest excess capital? We want to invest with managements that measure themselves against per-share metrics, not just the total size of the enterprise they manage. Much of the research we read does not do a good job translating cash usage or generation into business value. Especially today, with near-zero interest rates, when a company is generating lots of cash and an analyst represents that in a model by simply growing the cash balance, then sets a value estimate based on a P/E, they are valuing that cash at pennies on the dollar.

Q: What makes your investment management different from that of others?

A: There are a couple of things in our firm structure that I believe differentiate us. First, we have career analysts that can achieve the same level of success as our portfolio managers. Many firms talk about how their superior research allows them to succeed, but then they economically encourage their best analysts to switch careers. Second, all we do at Oakmark (and Harris Associates, Oakmark’s advisor) is value investing. I think many firms are seduced by the attraction of offering both value and growth funds. That might help smooth the advisor’s earnings, but in the end, I believe that having two opposite approaches working together simply encourages style drift at the times when it is most important to maintain discipline.

Further, though we follow a very disciplined approach, we allow what we believe is an appropriate level of creativity in how value is defined for each company we analyze. For some companies book value is a good measure of value, for some sales, for others cash flow. Sometimes you need to look at discretionary cash flow before advertising or R&D to find hidden value. By not requiring that the same summary statistic (P/E for example) be used to define value for every company, I believe we meaningfully expand our selection universe.

Last, we are different from most fund managers in how we think about risk. To most managers, and most fund evaluation services, risk is defined either as volatility of returns or deviation from the S&P returns. We define risk as losing money. Though Oakmark returns in any given year may be somewhat more volatile than other funds, or may deviate significantly from the S&P return, I consider Oakmark to be a below-average risk fund. The statistic I cite is that if you look at every year when the S&P lost money, Oakmark lost less.

Q: Can you explain the rationale behind the large exposure (28.6%) to the financial services sector in your portfolio?

A: We think financials are very cheap. An interesting stat I saw recently showed that the price/book for financials was 20% lower than the price/book for utilities, despite currently earning the same ROE. Plus, we consider current financials earnings to still be depressed because of legacy home mortgage losses and legal expenses. One thing many investors fear is that new regulations will make financials much more like electric utilities. It appears to us that the market has more than priced in that risk already. Another fear many investors have is that in a slow growth economy with little lending demand, growth will be hard to come by for this industry. We aren’t certain that robust growth should be ruled out as a possibility, but if the economy only has tepid growth, we believe financials should be able to return almost all their income to shareholders in dividends and share repurchase.

Q: Many of the companies you own are heavy repurchasers of their own stock. As companies repurchase significant percentages of their own stock yearly (an example being IBM), what does it mean for available amounts of stock in the future? Will there be a shortage of available shares? At the current pace IBM (IBM) will effectively buy the entire company back in 20 years. Or will companies have to shift to greater dividend increases as share counts decrease over time?

A: Clearly the individual who owns 1 share of IBM today, and holds it for 20 years, is not going to own 100% of IBM. Assuming the business value is static or increasing, using free cash flow to reduce the number of shares should result in an increase in the price of each remaining share. Though IBM in the past year purchased 5% of its stock with free cash flow, a rising share price should mean that the same amount of free cash in future years buys back a smaller number of shares. Effectively, if IBM buys 5% of its shares each year for the next 20 years it will not result in zero percent of its shares outstanding but rather 0.95 raised to the 20th power, or 36% of today’s share base. The individual who owns1% of the shares today would see their ownership increase to just under 3%, not 100%.

Q: With your PMV/relative approach to valuation, what adjustments do you make to your process to protect your portfolio against the risk that all assets might be overvalued in the market place?

A: There are two ways we introduce into our process protection against all assets being overvalued. First, when we look at transactions for comparables, we are skeptical of acquisitions that were done entirely for stock. A little over a decade ago one could have looked at stock acquisitions of Internet companies and concluded that many Internet companies were cheap. Effectively, one company with a stock it knew was grossly overvalued would issue stock to buy another that wasn’t quite as overvalued. By focusing on multiples that were paid in transactions where the buyer parted with cash, we had a much less frothy view of values.

The second thing we do is to always use several models to support our valuation estimate. One of those models is a dividend discount model that bases fair value off of earning a reasonable return in excess of what can be earned in risk-free securities. If going private transactions were occurring at prices that looked too expensive relative to our dividend discount models, we would not use those comparables to value public companies. Also, to protect against our dividend discount model producing excessive valuations, we put a floor on our risk-free rate. Recently we believed the bond market was overvalued and didn’t want our equity valuations to be dependent on bonds remaining overvalued.

Q: How do you personally try to improve your investing methodology on an ongoing basis?

A: First, we spend a lot of time analyzing our mistakes both statistically and qualitatively. Discovering a pattern in mistakes has led us to some tweaks in our process. Additionally, I read a lot of the material put out by our competitors to make sure they haven’t thought of something that we should also be doing. Further, I am actively involved in the Applied Securities Analysis Program at the University of Wisconsin, and the value investing program at Columbia University. If there are changes in how investing is being taught in the best business schools, I want to be aware of it.

I think another way we improve is by keeping a good balance on our research team between experienced veterans and enthusiastic rookies. At Oakmark we have never had as strong a group of young analysts as we have today. And though the experience gained over a long career gives one the advantage of frequently believing, “I think I’ve seen this movie before”, the value of that experience would not be maximized without the energy that comes with great young analysts. They make me better, and I think I also make them better.

Q: What percentage of your portfolio do you intentionally keep in cash to take advantage of the occasional "event”-driven stock selling?

A: I like to have enough cash to initiate a full new position (about 2% of the portfolio for Oakmark) without having to first sell something we own. The rest of the cash we hold is to provide liquidity for potential redemptions so that we aren’t the forced seller someone else is taking advantage of.

Q: You obviously buy large quantities of stock to fill a position – do you buy in tranches, i.e. you have in mind a certain amount you’d like to invest and then buy a percentage and wait for the price to go down/up to purchase an additional tranche?

A: Strategically, for most new stocks in Oakmark I will target a 1% position size, which will get increased toward 2% as the stock gets cheaper, or as we gain further evidence that our forecasts are likely to be achieved. Tactically, how we purchase the orders I give our traders, is entirely up to them. I’m not a trader. Best case, if I took more control of the tactics, I’d be wasting a lot of my time. Worst case, I’d lessen the quality of executions we now get by leaving the decisions to the professionals. It puzzles me why so many fund managers aren’t willing to delegate trading tactics to their own professional traders.

Q: What do you do with distributions (dividends, etc.) – reinvest, mix in with your cash for future purchase or other?

A: We treat dividend payments the same as subscriptions to the Fund. Our first responsibility is to make sure we have a prudent level of cash – defensively that means enough to handle unanticipated redemptions without becoming a forced seller; offensively, enough to take advantage of a forced seller without first having to sell something we already own. The second responsibility is to make sure the portfolio weightings are consistent with how attractively priced we believe each stock is. When new capital is received, we redeploy it into the stocks that we deem most deserving of increased portfolio weightings.

Q: I used to think that I could select active managers, because I seemed to consistently realize 1% to 2% better results than the corresponding indexes for a very long stretch of time. But more recently, I started learning about "factor investing," one of the "factors" being low volatility. And it turns out that I had systematically tended to favor low volatility funds over my investing history (not the only criterion, but one of my favorites). The reason is that I had observed over time that if I selected funds that had both modest trailing outperformance and lower than average volatility, the outperformance of those funds seem to have more persistence than the ones with trailing outperformance and higher volatility.

Now I am wondering whether all I was doing was "harvesting the low volatility premium" as people would say nowadays, rather than exhibiting skill at selecting a manager.

(My second favorite criterion is to read manager comments carefully and make a qualitative judgment about whether the manager seems to know what he is talking about. However, I would have a hard time writing down my recipe for doing that. Whether that has made any difference, I have no idea.)

A: In theory, you’d expect lower risk to mean you have to accept lower return. If you were achieving modest outperformance with lower than average risk, you were doing a doubly good job. If someone tries to diminish that accomplishment by saying you just captured a low volatility premium, I think they are mistaken. You achieved an outcome academics say is impossible – higher returns with lower risk. It seems logical to me that your approach was successful because so many good managers achieve their results by first focusing on protecting their capital, and only then thinking about upside.

I also agree with you that reading manager commentary is an underutilized resource for manager selection. You get a very different perspective from reading a manager’s thoughts than you do by just analyzing historical performance. I believe that it is difficult to select good managers without understanding how they approach investing. Without that, you’ll never have the conviction to stay invested through the underperforming periods. That’s why we at Oakmark put so much time into writing quarterlies that attempt to explain our actions in a manner that sheds more light on our investment philosophy.

Q: Bill, your approach seems purely Grahamian rather than Buffett's variation on Graham's work. In light of the constant tax bite of selling when a stock reaches intrinsic value, are you ever tempted to follow Buffett and continue holding it so long as the business is operating well?

A: I think we analyze companies much more like Buffett than Graham. We assign a lot of value to intangible assets, such as brands or patents, as opposed to the focus on tangible assets that Graham utilized. But unlike Buffett, we do sell stocks when we believe they exceed 90% of value. You are right that the downside of our approach is that we don’t defer taxes as long as Buffett does. We believe that is more than offset by getting our sales proceeds (net of long term capital gains taxes) invested in stocks we believe are selling at 60% of value instead of 90%.

Q: Mr. Nygren, you have been quoted as saying you sell when a company is fairly valued rather than waiting for it to become over-valued because you would not buy a company that is merely fairly valued. One might argue that the problem with that argument is that the only company which would meet that buy criteria is one which has been undervalued sufficiently to be in your portfolio and then rises to be fairly valued – that is, only the company you are selling. So, it would not be a feasible buy criterion, but could be a good tweak to your sell criteria. Since "the growth guys" generally overpay, and since there is evidence that momentum can be profitably combined with value investing, do you think this counterargument has any merit? (I have been an Oakmark Select investor for many years and greatly appreciate what you have done for me!)

A: Thank you for the kind comments. To me, a basic part of being a value investor is that, all else equal, a higher price decreases a stock’s attractiveness and vice-versa. I think it is dangerous to attempt to marry a value approach with a price momentum approach. Momentum of analyst’s assessment of fundamentals, however, is something that can be incorporated. Our history has shown, and I believe other value firms have also experienced, that analyst sell targets tend to show an anchoring bias. By that I mean that the magnitude of the positive and negative adjustments to targets based on fundamental developments is less than would occur if the stock was being looked at with a clean slate. Before I buy stocks where our estimates of value have been in decline, or sell stocks where our value estimates have been rising, I will really push our analysts to make sure they have fully incorporated all recent news into their targets

Individual Stocks

Q: -What are your thoughts on Discover Financial Services (DFS) as a worthy investment both short term and long term?

-What do you think of an investment in SandRidge Mississippian Trust II (SDR) or SandRidge Mississippian Trust I (SDT) now?

-Do you think Blackberry (BBRY) can pull off a turnaround, or do you think its value is simply tied to its intellectual property? If you were to assign Blackberry a hand value currently, what would it be? Something like a 16, or a 19? In dollar terms, what do you think their true fair market value is?

A: Sorry, but we don’t comment on stocks we don’t own, and we don’t own any of these.

Q: Could you explain your investment logic behind National Oilwell Varco (NOV)? What are your expectations for the oil industry in general?

A: We don’t believe we are very good at forecasting commodity prices, including oil. Because of that, unless prices have strayed far from what users and producers suggest is a market clearing price, we usually just use the futures market as our best guess of future prices. Most oil stocks look cheap to us based on the spot price of around $100 per barrel. The group that looks cheap based on a long term price in the $70s, which is where long dated futures now trade, is much smaller.

Our thoughts on National Oilwell have changed little from when we bought it last quarter. This was the summary of our rationale published in the Oakmark quarterly report to shareholders: “National Oilwell is one of the world’s largest providers of equipment for oil and gas drilling. Drill rig equipment accounts for about half its sales with the other half a diverse assortment of pipes, pumps, tools, consumables and a distribution business. Last year the stock reached $90, which was 14 times earnings plus amortization. Earnings in the first half of this year are expected to be down about 5%, primarily due to decreased drilling caused by lower natural gas prices. Despite the relatively small dip in earnings, the stock fell 30% to a low of $63 this past quarter. We expect earnings to begin to recover later this year, and we believe that next year could be the most profitable in the company’s history. Earnings growth should be led by a rebound in the global land rig count, continued strong deepwater equipment orders and the benefits reaped from several meaningful acquisitions. Though National Oilwell’s stock has recovered somewhat, it is still priced at less than 10 times estimated 2014 earnings plus amortization. Given that National Oilwell controls more than 50% of the deepwater equipment market and the company’s very high returns on tangible capital, we believe the current valuation is attractive.”

Q: I would like to know what is your thesis for AIG (AIG)? What did you see that made you think it was worth a big bet in your fund's holdings? What are the key points you look at when you invest in an insurance company?

A: This is what we wrote in the Oakmark quarterly in June, 2012 when we first purchased AIG: “AIG is a large insurance company operating in both property and casualty (Chartis) and life (SunAmerica). It is a poster child of the financial crisis, having required over $180 billion in government aid, and the government still owns over half of its outstanding shares. While the rescue measures still dampen its current valuation, we believe AIG has made remarkable progress under the leadership of CEO Robert Benmosche. The government loans have been completely repaid, and the stock currently trades above the government’s breakeven point of $29. Two years ago, we found it almost impossible to estimate the value of AIG’s equity. The analysis involved guessing at proceeds from sales of businesses and valuing large, opaque, levered loan portfolios. Today the analysis is the same as it would be for any insurer: What is its future earnings outlook? How good are its reserves? How will its capital be invested? Chartis went through a difficult period of writing unprofitable business just to grow revenues. That has stopped, and we believe that for the past several years Chartis has focused on only writing profitable business even if growth suffers. Reserves have been boosted to a level that we think is consistent with other high-quality insurers. Capital is being invested primarily in share repurchase -- with AIG selling at just over half of book, this is nicely accretive to the company’s per-share book value. We believe that AIG should earn over $3 per share this year and is on track to earn in excess of $5 per share within a few years. We believe that AIG is priced as if its future looks like its past. We expect the current discount to other insurers will diminish as the memory of the financial crisis fades.”

A little more than a year later not much has changed in our thinking. We don’t see any reason that AIG should not be worth at least book value. As with any insurer, we are focused on reserve adequacy, and believe AIG’s appear at least as strong as industry average. Also, we like to see a willingness to walk away from business when pricing is viewed as inadequate, which AIG has demonstrated. Too many insurers focus on revenue growth goals which often lead to bad underwriting.

Q: Please explain your views on DirecTV (DTV). How badly would DirecTV be hurt by losing the NFL Ticket? Regarding DTV, what is your view on its maintenance capex in relation to its stated current capex (growth vs. maintenance)? And how do you see the maintenance capex in the future (five years from now)?

A: DirecTV appears to be an inexpensive stock, selling at about 11x consensus estimates for 2014 earnings, compared to about 15x for the S&P 500. Most of its value comes from its US subscribers. The US market is mature, producing small earnings growth, but great cash generation. The next biggest piece of value is its Latin American operation, which is growing much more rapidly because multichannel penetration is still quite low. One of the things we like best about DirecTV is management’s approach to its capital structure. They believe that maintaining debt at 2.5x EBITDA maximizes long term value. As long as they believe the stock is undervalued, all capital in excess of the target leverage is used to repurchase shares, unless higher value opportunities arise. (As an aside, we strongly believe this should be the hurdle all managements use when evaluating acquisitions. Too often we see managements touting an acquisition as EPS accretive. Especially with near-zero interest rates, EPS accretive is not nearly a high enough hurdle. More accretive than share repurchase is a much more appropriate hurdle.)

Historically, DirecTV generated less cash than it reported as earnings, because with a growing subscriber base, it had to spend much more than its depreciation. That is still true to some extent in Latin America, but on a total company basis, spending is now in line with depreciation, so almost 100% of earnings could be returned to the owners.

Finally, DirecTV has always exclusively offered the NFL Season Ticket package, an expensive programming option that allows viewers to watch all out-of-market NFL games. DirecTV loses money on this offering, but it has helped in retention of customers that are high end sports fanatics. With the contract up for renewal next year, there has been some speculation that Google might bid a crazy price to replace DirecTV for the Ticket. I’m sure there is some dollar number at which the NFL would be willing to replace DirecTV, but the league realizes that DirecTV has been a good partner for getting broader distribution of their product. Few homes have AV systems for watching Internet TV, especially in HD, and even fewer have the bandwidth to allow simultaneous streaming of multiple games, which is what NFL Ticket viewers do. I think the qualitative cost to the NFL would be high to give the contract to Google. More likely, I think, is that the NFL might maximize revenue by allowing multiple providers to offer the Ticket rather than giving DirecTV exclusivity. In the end, if DirecTV loses the contract or loses exclusivity, there would be an immediate financial benefit which may or may not be offset by subscriber losses. In short, I don’t think the outcome matters much to DirecTV’s business value.

Q: How big is the threat of Google (GOOG) to Omnicom Group (OMC)?

A: Corporate advertising budgets are continuing to grow in line with sales as brands and consumer awareness have remained as important as ever. Advertising on-line has been growing much faster, from a small base, than traditional media advertising. One of the reasons we like Omnicom is because of its strong presence in on-line advertising. To the extent Google can make on-line advertising even more efficient, that should accelerate the market share shift to on-line, but should not hurt Omnicom.

General Market

Q: With the Fed tapering probably happening in a few months, what do you think will be the effect on the financial sector's stocks?

A: We are bottom-up investors, meaning we spend almost all our analytic time examining individual companies as opposed to trying to forecast macro factors. My first reaction is that I’m not certain that tapering will be as important to the markets as has been suggested by the financial media. The Fed has been an active buyer of bonds in about the same magnitude as the government has been deficit spending. Since the deficit is now declining, it seems to me that the Fed needs to lessen its purchases to not increase the government’s net impact on the bond market. More specifically to financial stocks, I believe that because the industry has become less levered and has shortened the duration of its assets, the group would likely see earnings rise if rates increased. With financial P/Es being so far below the market multiple, higher EPS may allow the group to increase in price even as rates also rise.

Q: You seem to think that the market is traded at a reasonable P/E ratio. Did you consider that earnings might be inflated by the historical high profit margins?

A: We have definitely considered that. Our opinion is that most of the increase in profit margins from historical averages is structural. Factors that, to us, suggest today’s higher margins are more than cyclical include: less profit from metal bending (low margin) more from intellectual property (high margin), less manufacturing more services, less US more International, and lower tax rates.

Miscellaneous

Q: Who is your all-time favorite investor and why?

A: I have tremendous admiration for the great value investors such as John Templeton and Warren Buffett. They followed a philosophy that makes sense to me, and their clarity of thought makes their written works very educational. But I’d have to say the investor I most admire is Michael Steinhardt. Michael was one of the first and most successful hedge fund managers. His track record of compounding investor capital at 25% per year over 28 years is amazing. I wrote about Steinhardt in a shareholder letter five years ago explaining how we at Oakmark have tried to incorporate some of his successful techniques (http://oakmarkservice.com/reports/2008_q1/comment1.htm). His insistence on having a “variant perception” (understanding how his point of view differed from most investors) and his use of a clean slate when he felt out of synch are two ideas I find especially compelling.

Q: What is the biggest investment mistake you made while at Oakmark, what did you learn from it and how can other value investors apply this knowledge to their research and portfolio management process?

A: The most money we lost came from not anticipating the 2008 collapse in housing. We thought that housing was such a long duration asset, and the cost of housing was so dependent on interest rates, that low interest rates would allow house prices to stay stable at a higher level. I think it is natural when thinking of mistakes to first think about those investments that resulted in losses, but mistakes of omission can be even more costly to a portfolio than mistakes of commission. I don’t lose any sleep over watching a stock that we don’t own go way up from levels we didn’t think were attractive anyway. The most painful mistakes are when a stock meets our investment criteria but we don’t invest as much as we should have. So when I think of most costly mistakes, I think of buying Apple for less than $100 in January of 2009, a level from which it increased eightfold, but only getting half of a normal-sized position in Oakmark Fund, and not owning any in Oakmark Select. Those are the kind of mistakes that re-examination may help better prepare us for the next time.

Q: What are some good books to read for investing and portfolio allocation?

A: .Anything written by Warren Buffett. I’ve also enjoyed the books that dedicate one chapter each to a group of successful managers – books like John Train’s Money Masters or Jack Schwager’s Wizards series. In those books, I especially find it useful to read about investors that use different approaches than we do. Though we focus on different variables, the similarity across successful investors of traits like discipline and passion is remarkable.

Q: Over the years that you have been in the business, upon reflection where do you think you have found the most "valuable" ideas?

A: Almost by definition, the stocks selling at the biggest discounts to value have to come from areas other investors aren’t looking, or where investors are so focused on short term negatives that they ignore long term opportunity. The stocks or sectors that leads one to are always changing, but the idea that the best opportunities are in places others are worried about or ignoring is almost fact rather than opinion. Among those cheap stocks, the best long-term performers have been those with managements that behaved like owners. When you own stocks for as long as we do, 5 years on average, the value additions that come from the unexpected opportunistic transactions management initiates can be very meaningful.

Q: What was the most valuable idea in your career and where was it found?

A: My best stock recommendation, by far, was Liberty Media. We bought it when it was first spun out from Telecommunications, Inc. in 1991. I found it because I regularly looked at spinoffs, believing that newly traded stocks had a higher probability of being misvalued than those with long trading histories. The stock was a hodge-podge of minority interest investments in cable TV systems and programming. It was levered, had no earnings, dividends or book value. There weren’t many screens that produced Liberty as a potentially cheap stock. But doing a tedious piece-by-piece valuation of each asset suggested that Liberty’s assets could be worth 3x the amount they were on the books for. The terms of its debt and preferred were so favorable that the liabilities appeared meaningfully overstated. Our guess of the per-share value was multiples of the value of the Telecommunications stock that needed to be exchanged to get the new Liberty shares. So few investors took advantage of this unusual exchange that we ended up owning much more of the company, 20%, than we had expected. Seven years later, when ATT bought Telecommunications and Liberty, we had made something like 20x our original investment. I think it is much harder to find similar values today than it was 20 years ago because the asset-by-asset valuation methodology for companies that don’t make sense on typical metrics is now much more widely used.

Q: What would you say was the one book, teacher, job or whichever, that shaped your stock picking philosophy?

A: When I was in high school I read all the investment books our local public library branch had. That’s less heroic than it sounds because investing was not a popular topic in the 70s. The book that made the most sense to me was Ben Graham’s Intelligent Investor. I was raised by parents that were very value conscious consumers, so the idea that you could succeed by buying stocks like you bought groceries and clothing, made perfect sense to me. The teacher that I learned the most from was Professor Steve Hawk. Steve started the Applied Securities Analysis Program at the University of Wisconsin. That program has launched hundreds of successful investment industry careers. Steve taught with a blend of practical and academic experience that is sadly lacking at most schools today. He always told his students that there are lots of investment approaches that could be successful, but that it is up to each individual to find the approach that best suits him or her. Being a value focused consumer was so deeply ingrained in me that when I learned about value investing I knew I had found the approach I was most likely to succeed with.

Q: I am an investor in both OAKMX and OAKIX and am very appreciative of you and your colleagues' work as fund managers. My question: Do you think it is possible for an intelligent amateur investor to select an active fund manager who is more likely than not to outperform the average fund or benchmark in his category going forward? If so, how do you think the investor can do that?

A: I believe the answer is yes. If I were trying to identify such a manager I would look for the same things we look for in the management teams of companies we invest in: an individual track record of success, an organization that has a track record of creating successes, a rational disciplined investment philosophy, a strong team, and good economic alignment with the shareholders (large personal investment in the fund). That said, identifying successful managers is not nearly as difficult as it is to stay invested with those managers long enough to reap the fruits from their labors. Unfortunately, the average mutual fund investor has underperformed the average of the funds they invest in because of poorly timed entrances and exits. I think one is unlikely to achieve good (market beating) results unless fund purchases are limited to those where one believes in the people, process and philosophy, and where one has the strength of conviction to not panic and sell just because of disappointing short term performance. If the only reason for buying a fund is good recent performance, then there will be no conviction to stay the course when times get tough.

Q: How do you identify undervalued companies? How much time does it take you to transform a checklist passer into an investment reality (i.e. from detecting the opportunity until it is in your portfolio)?

A: We compute our estimates of business value and look for companies selling at large discounts. When we value a stock, we first value the unlevered company, and then adjust for debt or cash to obtain a per-share value. Our favorite metric to base a valuation off of is the cash acquisition price of a similar company. In the absence of good comparable acquisitions we will consider as inputs acquisitions of businesses with similar characteristics from other industries, public market comparables, discounted cash flow models and so on. Our goal is to determine the maximum price an all cash buyer could pay to own the entire business and still earn an adequate return on their investment.

The time it takes can vary broadly. Sometimes an idea is so clear that within a week of starting work on it one concludes it should be purchased. Other times a stock can remain on our “research underway” list for years with no conclusion. I’ve found that our best ideas typically don’t linger very long in the “in process” stage. As Buffett says, it’s OK to decide a stock belongs in the “too tough pile.”

Q: As you've been investing for many years, your circle of competence grows and grows. What are some leading qualities of companies that finally attract you to make a purchase? Furthermore, when you analyze a company, what are some commonalities in the way you value them? For example, you may project growth for three years, then the company matures.

A: Most of our opportunities come from the very long term time horizon we use. When we model a company our analysts will do full financials two years out, then use an annual per-share value growth rate for the following five years, effectively giving us a 7 year forecast horizon. Most analysts use at most a two year horizon, and most stocks are traded based on even shorter horizons. A typical opportunity for us comes from negative news that we believe is cyclical that the market treats as if it is permanent. As an example, given weak economies today in most of Europe, current European car sales are beneath the level necessary to keep the car population flat. Many analysts are calculating business values based on static European sales, and conclude that auto businesses are appropriately valued. We don’t believe that Europe’s car population is going to go into secular decline. Therefore, we base our valuations off of sales much higher than are occurring today. As a result, we conclude that many global auto companies are cheap.

Q: What are some qualitative characteristics that you look for when buying shares in a company?

A: We look at many of the same characteristics other long term investors look at – competitive landscape, strength of brands, risk of disruption, and so on. But there are two questions that I think we pay more attention to than most investors do: Does forecasted growth require capital investment or will excess cash be generated? And how does management evaluate how to raise needed capital or invest excess capital? We want to invest with managements that measure themselves against per-share metrics, not just the total size of the enterprise they manage. Much of the research we read does not do a good job translating cash usage or generation into business value. Especially today, with near-zero interest rates, when a company is generating lots of cash and an analyst represents that in a model by simply growing the cash balance, then sets a value estimate based on a P/E, they are valuing that cash at pennies on the dollar.

Q: What makes your investment management different from that of others?

A: There are a couple of things in our firm structure that I believe differentiate us. First, we have career analysts that can achieve the same level of success as our portfolio managers. Many firms talk about how their superior research allows them to succeed, but then they economically encourage their best analysts to switch careers. Second, all we do at Oakmark (and Harris Associates, Oakmark’s advisor) is value investing. I think many firms are seduced by the attraction of offering both value and growth funds. That might help smooth the advisor’s earnings, but in the end, I believe that having two opposite approaches working together simply encourages style drift at the times when it is most important to maintain discipline.

Further, though we follow a very disciplined approach, we allow what we believe is an appropriate level of creativity in how value is defined for each company we analyze. For some companies book value is a good measure of value, for some sales, for others cash flow. Sometimes you need to look at discretionary cash flow before advertising or R&D to find hidden value. By not requiring that the same summary statistic (P/E for example) be used to define value for every company, I believe we meaningfully expand our selection universe.

Last, we are different from most fund managers in how we think about risk. To most managers, and most fund evaluation services, risk is defined either as volatility of returns or deviation from the S&P returns. We define risk as losing money. Though Oakmark returns in any given year may be somewhat more volatile than other funds, or may deviate significantly from the S&P return, I consider Oakmark to be a below-average risk fund. The statistic I cite is that if you look at every year when the S&P lost money, Oakmark lost less.

Q: Can you explain the rationale behind the large exposure (28.6%) to the financial services sector in your portfolio?

A: We think financials are very cheap. An interesting stat I saw recently showed that the price/book for financials was 20% lower than the price/book for utilities, despite currently earning the same ROE. Plus, we consider current financials earnings to still be depressed because of legacy home mortgage losses and legal expenses. One thing many investors fear is that new regulations will make financials much more like electric utilities. It appears to us that the market has more than priced in that risk already. Another fear many investors have is that in a slow growth economy with little lending demand, growth will be hard to come by for this industry. We aren’t certain that robust growth should be ruled out as a possibility, but if the economy only has tepid growth, we believe financials should be able to return almost all their income to shareholders in dividends and share repurchase.

Q: Many of the companies you own are heavy repurchasers of their own stock. As companies repurchase significant percentages of their own stock yearly (an example being IBM), what does it mean for available amounts of stock in the future? Will there be a shortage of available shares? At the current pace IBM (IBM) will effectively buy the entire company back in 20 years. Or will companies have to shift to greater dividend increases as share counts decrease over time?

A: Clearly the individual who owns 1 share of IBM today, and holds it for 20 years, is not going to own 100% of IBM. Assuming the business value is static or increasing, using free cash flow to reduce the number of shares should result in an increase in the price of each remaining share. Though IBM in the past year purchased 5% of its stock with free cash flow, a rising share price should mean that the same amount of free cash in future years buys back a smaller number of shares. Effectively, if IBM buys 5% of its shares each year for the next 20 years it will not result in zero percent of its shares outstanding but rather 0.95 raised to the 20th power, or 36% of today’s share base. The individual who owns1% of the shares today would see their ownership increase to just under 3%, not 100%.

Q: With your PMV/relative approach to valuation, what adjustments do you make to your process to protect your portfolio against the risk that all assets might be overvalued in the market place?

A: There are two ways we introduce into our process protection against all assets being overvalued. First, when we look at transactions for comparables, we are skeptical of acquisitions that were done entirely for stock. A little over a decade ago one could have looked at stock acquisitions of Internet companies and concluded that many Internet companies were cheap. Effectively, one company with a stock it knew was grossly overvalued would issue stock to buy another that wasn’t quite as overvalued. By focusing on multiples that were paid in transactions where the buyer parted with cash, we had a much less frothy view of values.

The second thing we do is to always use several models to support our valuation estimate. One of those models is a dividend discount model that bases fair value off of earning a reasonable return in excess of what can be earned in risk-free securities. If going private transactions were occurring at prices that looked too expensive relative to our dividend discount models, we would not use those comparables to value public companies. Also, to protect against our dividend discount model producing excessive valuations, we put a floor on our risk-free rate. Recently we believed the bond market was overvalued and didn’t want our equity valuations to be dependent on bonds remaining overvalued.

Q: How do you personally try to improve your investing methodology on an ongoing basis?

A: First, we spend a lot of time analyzing our mistakes both statistically and qualitatively. Discovering a pattern in mistakes has led us to some tweaks in our process. Additionally, I read a lot of the material put out by our competitors to make sure they haven’t thought of something that we should also be doing. Further, I am actively involved in the Applied Securities Analysis Program at the University of Wisconsin, and the value investing program at Columbia University. If there are changes in how investing is being taught in the best business schools, I want to be aware of it.

I think another way we improve is by keeping a good balance on our research team between experienced veterans and enthusiastic rookies. At Oakmark we have never had as strong a group of young analysts as we have today. And though the experience gained over a long career gives one the advantage of frequently believing, “I think I’ve seen this movie before”, the value of that experience would not be maximized without the energy that comes with great young analysts. They make me better, and I think I also make them better.

Q: What percentage of your portfolio do you intentionally keep in cash to take advantage of the occasional "event”-driven stock selling?

A: I like to have enough cash to initiate a full new position (about 2% of the portfolio for Oakmark) without having to first sell something we own. The rest of the cash we hold is to provide liquidity for potential redemptions so that we aren’t the forced seller someone else is taking advantage of.

Q: You obviously buy large quantities of stock to fill a position – do you buy in tranches, i.e. you have in mind a certain amount you’d like to invest and then buy a percentage and wait for the price to go down/up to purchase an additional tranche?

A: Strategically, for most new stocks in Oakmark I will target a 1% position size, which will get increased toward 2% as the stock gets cheaper, or as we gain further evidence that our forecasts are likely to be achieved. Tactically, how we purchase the orders I give our traders, is entirely up to them. I’m not a trader. Best case, if I took more control of the tactics, I’d be wasting a lot of my time. Worst case, I’d lessen the quality of executions we now get by leaving the decisions to the professionals. It puzzles me why so many fund managers aren’t willing to delegate trading tactics to their own professional traders.

Q: What do you do with distributions (dividends, etc.) – reinvest, mix in with your cash for future purchase or other?

A: We treat dividend payments the same as subscriptions to the Fund. Our first responsibility is to make sure we have a prudent level of cash – defensively that means enough to handle unanticipated redemptions without becoming a forced seller; offensively, enough to take advantage of a forced seller without first having to sell something we already own. The second responsibility is to make sure the portfolio weightings are consistent with how attractively priced we believe each stock is. When new capital is received, we redeploy it into the stocks that we deem most deserving of increased portfolio weightings.

Q: I used to think that I could select active managers, because I seemed to consistently realize 1% to 2% better results than the corresponding indexes for a very long stretch of time. But more recently, I started learning about "factor investing," one of the "factors" being low volatility. And it turns out that I had systematically tended to favor low volatility funds over my investing history (not the only criterion, but one of my favorites). The reason is that I had observed over time that if I selected funds that had both modest trailing outperformance and lower than average volatility, the outperformance of those funds seem to have more persistence than the ones with trailing outperformance and higher volatility.

Now I am wondering whether all I was doing was "harvesting the low volatility premium" as people would say nowadays, rather than exhibiting skill at selecting a manager.

(My second favorite criterion is to read manager comments carefully and make a qualitative judgment about whether the manager seems to know what he is talking about. However, I would have a hard time writing down my recipe for doing that. Whether that has made any difference, I have no idea.)

A: In theory, you’d expect lower risk to mean you have to accept lower return. If you were achieving modest outperformance with lower than average risk, you were doing a doubly good job. If someone tries to diminish that accomplishment by saying you just captured a low volatility premium, I think they are mistaken. You achieved an outcome academics say is impossible – higher returns with lower risk. It seems logical to me that your approach was successful because so many good managers achieve their results by first focusing on protecting their capital, and only then thinking about upside.

I also agree with you that reading manager commentary is an underutilized resource for manager selection. You get a very different perspective from reading a manager’s thoughts than you do by just analyzing historical performance. I believe that it is difficult to select good managers without understanding how they approach investing. Without that, you’ll never have the conviction to stay invested through the underperforming periods. That’s why we at Oakmark put so much time into writing quarterlies that attempt to explain our actions in a manner that sheds more light on our investment philosophy.

Q: Bill, your approach seems purely Grahamian rather than Buffett's variation on Graham's work. In light of the constant tax bite of selling when a stock reaches intrinsic value, are you ever tempted to follow Buffett and continue holding it so long as the business is operating well?

A: I think we analyze companies much more like Buffett than Graham. We assign a lot of value to intangible assets, such as brands or patents, as opposed to the focus on tangible assets that Graham utilized. But unlike Buffett, we do sell stocks when we believe they exceed 90% of value. You are right that the downside of our approach is that we don’t defer taxes as long as Buffett does. We believe that is more than offset by getting our sales proceeds (net of long term capital gains taxes) invested in stocks we believe are selling at 60% of value instead of 90%.

Q: Mr. Nygren, you have been quoted as saying you sell when a company is fairly valued rather than waiting for it to become over-valued because you would not buy a company that is merely fairly valued. One might argue that the problem with that argument is that the only company which would meet that buy criteria is one which has been undervalued sufficiently to be in your portfolio and then rises to be fairly valued – that is, only the company you are selling. So, it would not be a feasible buy criterion, but could be a good tweak to your sell criteria. Since "the growth guys" generally overpay, and since there is evidence that momentum can be profitably combined with value investing, do you think this counterargument has any merit? (I have been an Oakmark Select investor for many years and greatly appreciate what you have done for me!)

A: Thank you for the kind comments. To me, a basic part of being a value investor is that, all else equal, a higher price decreases a stock’s attractiveness and vice-versa. I think it is dangerous to attempt to marry a value approach with a price momentum approach. Momentum of analyst’s assessment of fundamentals, however, is something that can be incorporated. Our history has shown, and I believe other value firms have also experienced, that analyst sell targets tend to show an anchoring bias. By that I mean that the magnitude of the positive and negative adjustments to targets based on fundamental developments is less than would occur if the stock was being looked at with a clean slate. Before I buy stocks where our estimates of value have been in decline, or sell stocks where our value estimates have been rising, I will really push our analysts to make sure they have fully incorporated all recent news into their targets

Individual Stocks

Q: -What are your thoughts on Discover Financial Services (DFS) as a worthy investment both short term and long term?

-What do you think of an investment in SandRidge Mississippian Trust II (SDR) or SandRidge Mississippian Trust I (SDT) now?

-Do you think Blackberry (BBRY) can pull off a turnaround, or do you think its value is simply tied to its intellectual property? If you were to assign Blackberry a hand value currently, what would it be? Something like a 16, or a 19? In dollar terms, what do you think their true fair market value is?

A: Sorry, but we don’t comment on stocks we don’t own, and we don’t own any of these.

Q: Could you explain your investment logic behind National Oilwell Varco (NOV)? What are your expectations for the oil industry in general?

A: We don’t believe we are very good at forecasting commodity prices, including oil. Because of that, unless prices have strayed far from what users and producers suggest is a market clearing price, we usually just use the futures market as our best guess of future prices. Most oil stocks look cheap to us based on the spot price of around $100 per barrel. The group that looks cheap based on a long term price in the $70s, which is where long dated futures now trade, is much smaller.

Our thoughts on National Oilwell have changed little from when we bought it last quarter. This was the summary of our rationale published in the Oakmark quarterly report to shareholders: “National Oilwell is one of the world’s largest providers of equipment for oil and gas drilling. Drill rig equipment accounts for about half its sales with the other half a diverse assortment of pipes, pumps, tools, consumables and a distribution business. Last year the stock reached $90, which was 14 times earnings plus amortization. Earnings in the first half of this year are expected to be down about 5%, primarily due to decreased drilling caused by lower natural gas prices. Despite the relatively small dip in earnings, the stock fell 30% to a low of $63 this past quarter. We expect earnings to begin to recover later this year, and we believe that next year could be the most profitable in the company’s history. Earnings growth should be led by a rebound in the global land rig count, continued strong deepwater equipment orders and the benefits reaped from several meaningful acquisitions. Though National Oilwell’s stock has recovered somewhat, it is still priced at less than 10 times estimated 2014 earnings plus amortization. Given that National Oilwell controls more than 50% of the deepwater equipment market and the company’s very high returns on tangible capital, we believe the current valuation is attractive.”

Q: I would like to know what is your thesis for AIG (AIG)? What did you see that made you think it was worth a big bet in your fund's holdings? What are the key points you look at when you invest in an insurance company?

A: This is what we wrote in the Oakmark quarterly in June, 2012 when we first purchased AIG: “AIG is a large insurance company operating in both property and casualty (Chartis) and life (SunAmerica). It is a poster child of the financial crisis, having required over $180 billion in government aid, and the government still owns over half of its outstanding shares. While the rescue measures still dampen its current valuation, we believe AIG has made remarkable progress under the leadership of CEO Robert Benmosche. The government loans have been completely repaid, and the stock currently trades above the government’s breakeven point of $29. Two years ago, we found it almost impossible to estimate the value of AIG’s equity. The analysis involved guessing at proceeds from sales of businesses and valuing large, opaque, levered loan portfolios. Today the analysis is the same as it would be for any insurer: What is its future earnings outlook? How good are its reserves? How will its capital be invested? Chartis went through a difficult period of writing unprofitable business just to grow revenues. That has stopped, and we believe that for the past several years Chartis has focused on only writing profitable business even if growth suffers. Reserves have been boosted to a level that we think is consistent with other high-quality insurers. Capital is being invested primarily in share repurchase -- with AIG selling at just over half of book, this is nicely accretive to the company’s per-share book value. We believe that AIG should earn over $3 per share this year and is on track to earn in excess of $5 per share within a few years. We believe that AIG is priced as if its future looks like its past. We expect the current discount to other insurers will diminish as the memory of the financial crisis fades.”

A little more than a year later not much has changed in our thinking. We don’t see any reason that AIG should not be worth at least book value. As with any insurer, we are focused on reserve adequacy, and believe AIG’s appear at least as strong as industry average. Also, we like to see a willingness to walk away from business when pricing is viewed as inadequate, which AIG has demonstrated. Too many insurers focus on revenue growth goals which often lead to bad underwriting.

Q: Please explain your views on DirecTV (DTV). How badly would DirecTV be hurt by losing the NFL Ticket? Regarding DTV, what is your view on its maintenance capex in relation to its stated current capex (growth vs. maintenance)? And how do you see the maintenance capex in the future (five years from now)?

A: DirecTV appears to be an inexpensive stock, selling at about 11x consensus estimates for 2014 earnings, compared to about 15x for the S&P 500. Most of its value comes from its US subscribers. The US market is mature, producing small earnings growth, but great cash generation. The next biggest piece of value is its Latin American operation, which is growing much more rapidly because multichannel penetration is still quite low. One of the things we like best about DirecTV is management’s approach to its capital structure. They believe that maintaining debt at 2.5x EBITDA maximizes long term value. As long as they believe the stock is undervalued, all capital in excess of the target leverage is used to repurchase shares, unless higher value opportunities arise. (As an aside, we strongly believe this should be the hurdle all managements use when evaluating acquisitions. Too often we see managements touting an acquisition as EPS accretive. Especially with near-zero interest rates, EPS accretive is not nearly a high enough hurdle. More accretive than share repurchase is a much more appropriate hurdle.)

Historically, DirecTV generated less cash than it reported as earnings, because with a growing subscriber base, it had to spend much more than its depreciation. That is still true to some extent in Latin America, but on a total company basis, spending is now in line with depreciation, so almost 100% of earnings could be returned to the owners.

Finally, DirecTV has always exclusively offered the NFL Season Ticket package, an expensive programming option that allows viewers to watch all out-of-market NFL games. DirecTV loses money on this offering, but it has helped in retention of customers that are high end sports fanatics. With the contract up for renewal next year, there has been some speculation that Google might bid a crazy price to replace DirecTV for the Ticket. I’m sure there is some dollar number at which the NFL would be willing to replace DirecTV, but the league realizes that DirecTV has been a good partner for getting broader distribution of their product. Few homes have AV systems for watching Internet TV, especially in HD, and even fewer have the bandwidth to allow simultaneous streaming of multiple games, which is what NFL Ticket viewers do. I think the qualitative cost to the NFL would be high to give the contract to Google. More likely, I think, is that the NFL might maximize revenue by allowing multiple providers to offer the Ticket rather than giving DirecTV exclusivity. In the end, if DirecTV loses the contract or loses exclusivity, there would be an immediate financial benefit which may or may not be offset by subscriber losses. In short, I don’t think the outcome matters much to DirecTV’s business value.

Q: How big is the threat of Google (GOOG) to Omnicom Group (OMC)?

A: Corporate advertising budgets are continuing to grow in line with sales as brands and consumer awareness have remained as important as ever. Advertising on-line has been growing much faster, from a small base, than traditional media advertising. One of the reasons we like Omnicom is because of its strong presence in on-line advertising. To the extent Google can make on-line advertising even more efficient, that should accelerate the market share shift to on-line, but should not hurt Omnicom.

General Market

Q: With the Fed tapering probably happening in a few months, what do you think will be the effect on the financial sector's stocks?

A: We are bottom-up investors, meaning we spend almost all our analytic time examining individual companies as opposed to trying to forecast macro factors. My first reaction is that I’m not certain that tapering will be as important to the markets as has been suggested by the financial media. The Fed has been an active buyer of bonds in about the same magnitude as the government has been deficit spending. Since the deficit is now declining, it seems to me that the Fed needs to lessen its purchases to not increase the government’s net impact on the bond market. More specifically to financial stocks, I believe that because the industry has become less levered and has shortened the duration of its assets, the group would likely see earnings rise if rates increased. With financial P/Es being so far below the market multiple, higher EPS may allow the group to increase in price even as rates also rise.

Q: You seem to think that the market is traded at a reasonable P/E ratio. Did you consider that earnings might be inflated by the historical high profit margins?

A: We have definitely considered that. Our opinion is that most of the increase in profit margins from historical averages is structural. Factors that, to us, suggest today’s higher margins are more than cyclical include: less profit from metal bending (low margin) more from intellectual property (high margin), less manufacturing more services, less US more International, and lower tax rates.

Miscellaneous

Q: Who is your all-time favorite investor and why?

A: I have tremendous admiration for the great value investors such as John Templeton and Warren Buffett. They followed a philosophy that makes sense to me, and their clarity of thought makes their written works very educational. But I’d have to say the investor I most admire is Michael Steinhardt. Michael was one of the first and most successful hedge fund managers. His track record of compounding investor capital at 25% per year over 28 years is amazing. I wrote about Steinhardt in a shareholder letter five years ago explaining how we at Oakmark have tried to incorporate some of his successful techniques (http://oakmarkservice.com/reports/2008_q1/comment1.htm). His insistence on having a “variant perception” (understanding how his point of view differed from most investors) and his use of a clean slate when he felt out of synch are two ideas I find especially compelling.

Q: What is the biggest investment mistake you made while at Oakmark, what did you learn from it and how can other value investors apply this knowledge to their research and portfolio management process?

A: The most money we lost came from not anticipating the 2008 collapse in housing. We thought that housing was such a long duration asset, and the cost of housing was so dependent on interest rates, that low interest rates would allow house prices to stay stable at a higher level. I think it is natural when thinking of mistakes to first think about those investments that resulted in losses, but mistakes of omission can be even more costly to a portfolio than mistakes of commission. I don’t lose any sleep over watching a stock that we don’t own go way up from levels we didn’t think were attractive anyway. The most painful mistakes are when a stock meets our investment criteria but we don’t invest as much as we should have. So when I think of most costly mistakes, I think of buying Apple for less than $100 in January of 2009, a level from which it increased eightfold, but only getting half of a normal-sized position in Oakmark Fund, and not owning any in Oakmark Select. Those are the kind of mistakes that re-examination may help better prepare us for the next time.

Q: What are some good books to read for investing and portfolio allocation?

A: .Anything written by Warren Buffett. I’ve also enjoyed the books that dedicate one chapter each to a group of successful managers – books like John Train’s Money Masters or Jack Schwager’s Wizards series. In those books, I especially find it useful to read about investors that use different approaches than we do. Though we focus on different variables, the similarity across successful investors of traits like discipline and passion is remarkable.

Q: Over the years that you have been in the business, upon reflection where do you think you have found the most "valuable" ideas?