And one last repost with google's software glitches.

Saturday, November 9, 2013

Commodity Super Cycle Still Intact- Kaiser (repost)

And yet another repost due to google's software bugs

Kitco's Wyckokk- Central Banks Intervention Lead to Currency Wars (repost)

Repost due to errors with google software and proper broadcasting.

Although he just parrots the mainstream thinking, I would take up contention with Mr. Wyckoff of the 'negative' aspects of deflation. That said, some food for thought here.

Although he just parrots the mainstream thinking, I would take up contention with Mr. Wyckoff of the 'negative' aspects of deflation. That said, some food for thought here.

High Volume High- Nov. 7 Trading Day Edition (repost)

Reposting a few items due to items not broadcast with issues at Google.

The number of names here collapsed with supply hitting the market.

The number of names here collapsed with supply hitting the market.

Friday, November 8, 2013

How the Fed Learned to Stop Worrying and Love Easy Money

By Joseph Salerno for the Mises Institute

... It was not ultimately budget deficits that allowed Kennedy to initiate the corporatist planning and militarization of the U.S. economy that bore first fruit in the emergence of the American welfare-warfare state during Johnson’s Great Society and culminated in Nixon’s fascist New Economic Policy. The policy that facilitated Johnson’s simultaneous financing of extravagant expenditures on welfare programs and the military adventure in Vietnam and made conditions ripe for Nixon's imposition of wage and price controls was not newfangled functional finance but old-fashioned monetary inflation. As the historian of macroeconomic policy, Kenneth Weiher, has pointed out, it was not the much-vaunted “fiscal revolution” but the overlooked “monetary revolution” that took place during the Kennedy administration which turned out to be the predominant influence on the economic events of the 1960s and 1970s. As Weiher stated: “There was a revolution all right, but the most important change occurred at the Federal Reserve; however, 10 years passed before more than a handful of people caught on to what was happening.”

In the three years of the Kennedy administration the growth of the money

supply as measured by M2 averaged about 8 percent per year. If we take

the eleven

prior years going back to 1950, the rate of growth of M2 averaged 3.6

percent per year; if we go back four more years, to the first postwar

year of 1946,

the average annual rate of M2 growth over the fifteen-year period drops

to 3.3 percent.

There were basically two reasons why the role of monetary policy tended to be so grossly underplayed in the economic histories of this period. The first was that the new economists themselves, as unreconstructed Keynesians, uniformly denigrated the potency of monetary policy while touting the effectiveness of fiscal policy. Thus the Kennedy tax-cut bill, which did not even take effect until 1964, receives the lion’s share of the credit for stimulating the recovery from the 1960-1961 recession. Second, because most economists since the 1930s, including and especially those of Keynesian orientation, identified inflation with increases in the price level, and interpreted the 1.2-percent average annual rate of increase of the CPI during the period 1961-1963 as evidence of the absence of inflation

Despite the negligible increase in the CPI, however, the effects of the rapid, and initially unanticipated, monetary inflation were visible in credit markets as real interest rates trended steadily downward throughout the decade. Unfortunately, both Keynesian and central bank orthodoxies of the 1960s focused on the nominal interest rate as an important indicator of the degree of ease or restraint of monetary policy, making no allowance for the effect of inflationary expectations on the nominal interest rate. Consequently, neither the new economists nor the monetary authorities believed that monetary policy was “unduly” expansionary because short-term nominal interest rates rose from 1961 to 1963. Indeed, the new economists were quite pleased with monetary policy during this period, an attitude typified in Seymour Harris’s observation that “the [Federal Reserve] board provided the country with a reasonably easy money policy ...”

Given that monetary policy was indeed grossly inflationary during the Kennedy years, what accounts for the sudden and radical shift in Federal Reserve policy from the moderate inflationism under the Eisenhower administration? The answer is Kennedy and his new economists, who conducted a relentless and incessant campaign for easy money from the very beginning of his administration. This campaign took the form of repeated public utterances on the part of the president and his economic advisers, as well as direct presidential pressure on William McChesney Martin, who was chairman of the Fed under Eisenhower and continued in that position until 1970.

Kennedy and key members of his administration also doggedly prodded the Fed, both publicly and privately, to ease monetary policy, even threatening to terminate its independent status if it did not acquiesce. As early as his campaign for the presidency, Kennedy expressed his disappointment with the Fed’s tendency to resort to restrictive monetary policy to rein in inflation and his intention to break with such a policy. In April 1962, Kennedy petitioned Congress for a revision of the terms of the Fed chairmanship that would enable each president to nominate a new chairman at the beginning of his term. Heller, Treasury Secretary Dillon, and Treasury Undersecretary Roosa also weighed in with calls for the Fed to ease monetary policy. Despite some initial foot-dragging and repeated caveats that the Fed would only finance real economic growth and not budget deficits, Fed Chairman Martin ultimately capitulated to the insistent demands of Kennedy and the new economists for a cheap-money policy. In fact, in February 1961, the Fed abandoned its long-standing “bills-only doctrine,” which dictated that open market operations be conducted exclusively in the market for short-term securities. In doing so, the Fed was accommodating the administration’s request to reduce long-term interest rates by buying long-term securities while simultaneously selling short-term securities in order to nudge up short-term interest rates. This attempt to artificially twist the interest-rate structure — nicknamed Operation Twist — was devised by the new economists to accomplish two goals: to stimulate domestic business investment and new housing purchases and to discourage the outflow of domestic and encourage the inflow of foreign short-term capital as a means of mitigating the U.S. balance-of-payments deficit. Needless to say, this attempt to have one’s cake and eat it too — to pursue a domestic cheap money policy and to avoid its adverse consequences for the balance of payments — was a failure ...

Our conclusion then is that Kennedy and the new economists succeeded in wringing from the Fed precisely the inflationary monetary policy they desired and that this policy represented a radical break with the monetary policy pursued in the 1950s. This conclusion, which is certainly reflected in the money-supply growth rates cited above, also accords with the perceptions of the new economists themselves. Seymour Harris, long-time Kennedy economic adviser and chief academic consultant to the Kennedy Treasury, made this pellucidly clear in his book on the economic policies of the Kennedy years. Harris concluded that:

... It was not ultimately budget deficits that allowed Kennedy to initiate the corporatist planning and militarization of the U.S. economy that bore first fruit in the emergence of the American welfare-warfare state during Johnson’s Great Society and culminated in Nixon’s fascist New Economic Policy. The policy that facilitated Johnson’s simultaneous financing of extravagant expenditures on welfare programs and the military adventure in Vietnam and made conditions ripe for Nixon's imposition of wage and price controls was not newfangled functional finance but old-fashioned monetary inflation. As the historian of macroeconomic policy, Kenneth Weiher, has pointed out, it was not the much-vaunted “fiscal revolution” but the overlooked “monetary revolution” that took place during the Kennedy administration which turned out to be the predominant influence on the economic events of the 1960s and 1970s. As Weiher stated: “There was a revolution all right, but the most important change occurred at the Federal Reserve; however, 10 years passed before more than a handful of people caught on to what was happening.”

There were basically two reasons why the role of monetary policy tended to be so grossly underplayed in the economic histories of this period. The first was that the new economists themselves, as unreconstructed Keynesians, uniformly denigrated the potency of monetary policy while touting the effectiveness of fiscal policy. Thus the Kennedy tax-cut bill, which did not even take effect until 1964, receives the lion’s share of the credit for stimulating the recovery from the 1960-1961 recession. Second, because most economists since the 1930s, including and especially those of Keynesian orientation, identified inflation with increases in the price level, and interpreted the 1.2-percent average annual rate of increase of the CPI during the period 1961-1963 as evidence of the absence of inflation

Despite the negligible increase in the CPI, however, the effects of the rapid, and initially unanticipated, monetary inflation were visible in credit markets as real interest rates trended steadily downward throughout the decade. Unfortunately, both Keynesian and central bank orthodoxies of the 1960s focused on the nominal interest rate as an important indicator of the degree of ease or restraint of monetary policy, making no allowance for the effect of inflationary expectations on the nominal interest rate. Consequently, neither the new economists nor the monetary authorities believed that monetary policy was “unduly” expansionary because short-term nominal interest rates rose from 1961 to 1963. Indeed, the new economists were quite pleased with monetary policy during this period, an attitude typified in Seymour Harris’s observation that “the [Federal Reserve] board provided the country with a reasonably easy money policy ...”

Given that monetary policy was indeed grossly inflationary during the Kennedy years, what accounts for the sudden and radical shift in Federal Reserve policy from the moderate inflationism under the Eisenhower administration? The answer is Kennedy and his new economists, who conducted a relentless and incessant campaign for easy money from the very beginning of his administration. This campaign took the form of repeated public utterances on the part of the president and his economic advisers, as well as direct presidential pressure on William McChesney Martin, who was chairman of the Fed under Eisenhower and continued in that position until 1970.

Kennedy and key members of his administration also doggedly prodded the Fed, both publicly and privately, to ease monetary policy, even threatening to terminate its independent status if it did not acquiesce. As early as his campaign for the presidency, Kennedy expressed his disappointment with the Fed’s tendency to resort to restrictive monetary policy to rein in inflation and his intention to break with such a policy. In April 1962, Kennedy petitioned Congress for a revision of the terms of the Fed chairmanship that would enable each president to nominate a new chairman at the beginning of his term. Heller, Treasury Secretary Dillon, and Treasury Undersecretary Roosa also weighed in with calls for the Fed to ease monetary policy. Despite some initial foot-dragging and repeated caveats that the Fed would only finance real economic growth and not budget deficits, Fed Chairman Martin ultimately capitulated to the insistent demands of Kennedy and the new economists for a cheap-money policy. In fact, in February 1961, the Fed abandoned its long-standing “bills-only doctrine,” which dictated that open market operations be conducted exclusively in the market for short-term securities. In doing so, the Fed was accommodating the administration’s request to reduce long-term interest rates by buying long-term securities while simultaneously selling short-term securities in order to nudge up short-term interest rates. This attempt to artificially twist the interest-rate structure — nicknamed Operation Twist — was devised by the new economists to accomplish two goals: to stimulate domestic business investment and new housing purchases and to discourage the outflow of domestic and encourage the inflow of foreign short-term capital as a means of mitigating the U.S. balance-of-payments deficit. Needless to say, this attempt to have one’s cake and eat it too — to pursue a domestic cheap money policy and to avoid its adverse consequences for the balance of payments — was a failure ...

Our conclusion then is that Kennedy and the new economists succeeded in wringing from the Fed precisely the inflationary monetary policy they desired and that this policy represented a radical break with the monetary policy pursued in the 1950s. This conclusion, which is certainly reflected in the money-supply growth rates cited above, also accords with the perceptions of the new economists themselves. Seymour Harris, long-time Kennedy economic adviser and chief academic consultant to the Kennedy Treasury, made this pellucidly clear in his book on the economic policies of the Kennedy years. Harris concluded that:

In short, monetary policy under Kennedy was much more expansionist than under Eisenhower. ...Thus, inflationary monetary policy was the sine qua non for the regime of permanent budget deficits that was initiated in the early 1960s and continued uninterrupted almost to the end of the twentieth century. That private investment was able to continually expand concurrently with sharply increasing government spending on military and other programs was attributable in large measure to the fact that, during the Kennedy years, the Fed was induced to “cooperate” by routinely monetizing the cumulating budget deficits necessary to finance these programs.

Federal Reserve policy in 1961-1963 was not like that of 1952-1960. At the early stages of recovery in the 1950s, the Federal Reserve, overly sensitive to inflationary dangers, aborted recoveries. Whether the explanation was the growing conviction that inflation was no longer a threat, or whether it was an awareness that the Kennedy administration would not tolerate stifling monetary policies, the Federal Reserve made no serious attempts to deflate the economy after 1960. In fact, in 1963 Mr. Martin boasted of the large contributions made to expansion ...

Ghosts of Keynes

By William Anderson for the Mises Institute

When the U.S. economy dipped into an inflationary recession in 1969, Murray N. Rothbard in his introduction to the Second Edition of America’s Great Depression wrote that the Keynesian paradigm could not explain that phenomenon, but Austrian economics could explain what was happening. If Rothbard was correct — and he was — then one might believe Keynesian “economics” should have been deep-sixed permanently, given it could not explain what everyone saw happening.

Likewise, during the turbulent 1970s and 1980, the bouts of inflationary recessions grew worse and even die-hard political liberals such as ABC News’ economics correspondence, Dan Cordtz, bemoaned the fact that the “rules of economics” no longer seemed to apply. Those so-called rules were not laws of economics at all, but rather were dogma first given by John Maynard Keynes in his infamous work, The General Theory of Employment, Interest, and Money.

Joyous economists such as Arthur Laffer, who espoused a form of what he and others called “Supply Side Economics,” declared that Keynesian “economics” was discredited, perhaps for good. The advent of three more inflationary recessions, including the current downturn, should have resulted in the permanent death of Keynesianism, but, alas, it seems that the Keynesian paradigm is more influential than ever.

Exhibit A is President Barack Obama who in 2009 shortly after taking office declared that America would “spend its way out” of the current recession.

Exhibit B has been Obama’s recent announcement that he would nominate Janet Yellen to head the Federal Reserve System. Yellen, not surprisingly, is a True Believing Keynesian.

Exhibit C is the ongoing popularity of Paul Krugman, who has done more than any other person in the world to promote Keynesianism and to demand it be applied, chapter and verse, to the world economy.

Exhibit D has been the continuing Keynesian policies of the Federal Reserve and the central bank of Japan.

Academic economists who hold to the “market test” view of economics should be puzzled. Here is a paradigm that claims there cannot be an inflationary recession, yet all of the recessions that have wracked the U.S. economy in recent decades have been inflationary. Furthermore, despite the spending of more than a trillion dollars in the name of the Keynesian “stimulus,” the economy continues to founder, as unemployment rates remain stubbornly high and millions of workers either have abandoned their search for work or work in part-time jobs just to keep food on the table.

Given the fact that both the George W. Bush and Barack Obama administrations (not to mention Congress) have followed the Keynesian playbook, the sorry results should be enough to discredit Keynesianism, this time for good. Either a theory explains and predicts phenomena or it does not, and it should be clear that Keynesian theory has failed.

Alas, the academic “market test” really does not embrace the actual success or failure of a theory. It seems that many academic economists do not wish to be bothered by what happens in the real world. The vaunted “market test” is not about actual results, but is about what many economists are willing to accept as what they wish to be true and what politicians believe is good for their own electoral purposes.

The assumption that comes with attempting to apply Eugene Fama’s “Perfect Market Hypothesis” to academic economics presupposes that economists are interested only in what actually occurs. Furthermore, the belief presumes that when presented with a set of facts, academic economists will give the same analysis and not be influenced by partisan politics.

Given the interpretations that economists such as Krugman, Alan Blinder, and others have made in the aftermath of the disastrous first week of “ObamaCare,” not to mention their shilling for the Obama administration itself, the latter is clearly untrue. Furthermore, we see there are “gains from trade,” as politicians tend to flock to those economists who can offer the proverbial “quick fix” to whatever ails the economy, as being seen as doing something confers more political benefits than doing the right thing, which is to curb the power, scope, and influence of state power.

Even Krugman admits that the appearance of expertise has fueled the Keynesian bandwagon:

When the U.S. economy dipped into an inflationary recession in 1969, Murray N. Rothbard in his introduction to the Second Edition of America’s Great Depression wrote that the Keynesian paradigm could not explain that phenomenon, but Austrian economics could explain what was happening. If Rothbard was correct — and he was — then one might believe Keynesian “economics” should have been deep-sixed permanently, given it could not explain what everyone saw happening.

Likewise, during the turbulent 1970s and 1980, the bouts of inflationary recessions grew worse and even die-hard political liberals such as ABC News’ economics correspondence, Dan Cordtz, bemoaned the fact that the “rules of economics” no longer seemed to apply. Those so-called rules were not laws of economics at all, but rather were dogma first given by John Maynard Keynes in his infamous work, The General Theory of Employment, Interest, and Money.

Joyous economists such as Arthur Laffer, who espoused a form of what he and others called “Supply Side Economics,” declared that Keynesian “economics” was discredited, perhaps for good. The advent of three more inflationary recessions, including the current downturn, should have resulted in the permanent death of Keynesianism, but, alas, it seems that the Keynesian paradigm is more influential than ever.

Exhibit A is President Barack Obama who in 2009 shortly after taking office declared that America would “spend its way out” of the current recession.

Exhibit B has been Obama’s recent announcement that he would nominate Janet Yellen to head the Federal Reserve System. Yellen, not surprisingly, is a True Believing Keynesian.

Exhibit C is the ongoing popularity of Paul Krugman, who has done more than any other person in the world to promote Keynesianism and to demand it be applied, chapter and verse, to the world economy.

Exhibit D has been the continuing Keynesian policies of the Federal Reserve and the central bank of Japan.

Academic economists who hold to the “market test” view of economics should be puzzled. Here is a paradigm that claims there cannot be an inflationary recession, yet all of the recessions that have wracked the U.S. economy in recent decades have been inflationary. Furthermore, despite the spending of more than a trillion dollars in the name of the Keynesian “stimulus,” the economy continues to founder, as unemployment rates remain stubbornly high and millions of workers either have abandoned their search for work or work in part-time jobs just to keep food on the table.

Given the fact that both the George W. Bush and Barack Obama administrations (not to mention Congress) have followed the Keynesian playbook, the sorry results should be enough to discredit Keynesianism, this time for good. Either a theory explains and predicts phenomena or it does not, and it should be clear that Keynesian theory has failed.

Alas, the academic “market test” really does not embrace the actual success or failure of a theory. It seems that many academic economists do not wish to be bothered by what happens in the real world. The vaunted “market test” is not about actual results, but is about what many economists are willing to accept as what they wish to be true and what politicians believe is good for their own electoral purposes.

The assumption that comes with attempting to apply Eugene Fama’s “Perfect Market Hypothesis” to academic economics presupposes that economists are interested only in what actually occurs. Furthermore, the belief presumes that when presented with a set of facts, academic economists will give the same analysis and not be influenced by partisan politics.

Given the interpretations that economists such as Krugman, Alan Blinder, and others have made in the aftermath of the disastrous first week of “ObamaCare,” not to mention their shilling for the Obama administration itself, the latter is clearly untrue. Furthermore, we see there are “gains from trade,” as politicians tend to flock to those economists who can offer the proverbial “quick fix” to whatever ails the economy, as being seen as doing something confers more political benefits than doing the right thing, which is to curb the power, scope, and influence of state power.

Even Krugman admits that the appearance of expertise has fueled the Keynesian bandwagon:

In the 1930s you had a catastrophe, and if you were a public official or even just a layman looking for guidance and understanding, what did you get from institutionalists? Caricaturing, but only slightly, you got long, elliptical explanations that it all had deep historical roots and clearly there was no quick fix. Meanwhile, along came the Keynesians, who were model-oriented, and who basically said “Push this button” — increase G, and all will be well. And the experience of the wartime boom seemed to demonstrate that demand-side expansion did indeed work the way the Keynesians said it did.In the past five years politicians have been pushing “button G” and all is not well. Yet, in this age of unrestrained government, the Keynesian promise of prosperity springing from massive government spending is attractive to politicians, economists, and public intellectuals. That it only makes things worse is irrelevant and beside the point. If the economy falters, politicians and academic economists blame capitalism, not Keynesianism, and they get away with it.

Gold: Hold It Or Fold It?

By Peter Schiff

It's starting to feel like we are part of a giant poker game against the US government, whose hand is the true condition of the American economy. The government has become so good at bluffing that most people feel compelled to watch how the biggest players in the game react to determine their own investment strategy.

Unfortunately, this past month revealed that even pros like Goldman Sachs have no idea what sort of hand Washington is really hiding.

Goldman Bets Against Gold

A week into the government shutdown, Jeffrey Currie, head of commodities research at Goldman Sachs, declared that gold would be a "slam dunk sell" if Washington resolved the budget debate and raised the debt ceiling. The call was based on an underlying narrative that the US economy is experiencing a slow, but inevitable, recovery.

Taking this recovery as a foregone conclusion, conventional Wall Street analysts saw two clear choices for Washington. On the one hand, Congress could reach an agreement, raise the debt ceiling, and allow the recovery to continue. This would allegedly have been the final nail in the coffin of the safe-haven appeal of gold.

On the other hand, if no agreement were reached, the government would have been forced to default on its debt. This would have erased any signs of recovery and sent the economy spiraling back into a terrible recession - while boosting the gold price.

Goldman reasoned that Washington would never allow the latter to unfold and suggested investors prepare to short or sell gold.

While Washington did kick the debt can down the road as predicted, gold rallied 3% on the news - the complete opposite of expectations. That is, expectations outside of Euro Pacific.

Misreading the Signals

After seeing an investment theory crushed by reality, a rational investor would take a moment to reexamine his premises. In Goldman's case, this would mean second-guessing the conventional belief in an imminent or ongoing US economic recovery.

Yet, the day after Washington reached an agreement, Currie reaffirmed to Goldman's clients that his US economic outlook for 2014 is positive and that he believes gold faces "significant downside risks."

Currie must not have wanted to muddy his message by acknowledging that his original forecast was flat wrong. He did, however, hedge his statements by acknowledging that the Federal Reserve would likely hold off on tapering its stimulus until next year.

Major Wall Street investment houses have come to rely on the investing public's short-term memory to skate by on these bad calls. When the next forecast is issued, clients and subscribers quickly forget that Goldman was blindsided by the Fed's taper fakeout in September. [Read more about the taper fakeout in my previous Gold Letter.] That Currie accepted the government's new taper timeline within a month of being burned by the last shows how little stomach they have for sticking to the fundamentals - and how little accountability they face for getting it wrong.

Instead, major players like Goldman Sachs are betting their books on the government's fearless bluff. In the eyes of Wall Street, the economic indicators support this conclusion - inflation is subdued, GDP is growing!

The Bluff Exposed

I've been an outspoken critic of this official data for years. Over the course of my career, I have witnessed the government dramatically change the way it calculates inflation, GDP, and other statistics. While Washington's latest figures show a year-over-year CPI increase of just 1.2%, the private service ShadowStats, which recalculates the data along the lines that the government used to, finds that real consumer inflation is closer to 9%.

My guess is the true number lies somewhere in between, but that it would be much higher were the US not able to export much of its inflation abroad. The process works as follows: the Fed prints money (inflation) and uses it to buy Treasuries and mortgages. The government and banks, in turn, pass much of that money to consumers, who spend it on imported goods. The money then flows to foreign manufacturers of those products, who then sell it to their own central banks, who print their own currencies (inflation) to buy it. This money goes out to pay wages, rents, etc., which the recipients then spend on goods & services. Finally, the foreign central banks use the dollars they buy to purchase US Treasuries and mortgages, starting the cycle again.

It's a complicated relationship, but the end result is that inflation created in the US ultimately bids up consumer prices abroad and Treasury prices at home. In other words, our trading partners have to pay much more for goods & services while Americans get to borrow limitless money for next to nothing. The products our trading partners "sell" us increase the supply of goods available to American consumers while simultaneously decreasing the supply available to everyone else. That is what I mean by "exporting inflation," and the important thing to remember is that its result is to mask inflation at home and transfer wealth from emerging markets to the US.

(Click for source)

(Click for source)

The bluff gets worse. These understated CPI numbers distort real GDP, which would be lower if the true inflation rate were applied. The GDP calculations also include items like government expenditures, which are possible only because of money printing and not a result of any real economic production. Again, compare the official figure of 1-2% GDP growth in the second quarter of 2013 to ShadowStat's figure of negative 2%.

(Click for source)

(Click for source)

If investors can't bring themselves to question official data, there's another way to see through the government's bluff: look to foreign central banks, which are actively preparing for the day when the dollar is no longer the world's reserve currency.

The Bank of Italy recently affirmed that its gold reserves are essential to its economic independence, while the World Gold Council reported that this past year, European central banks held onto more of their gold reserves than ever before. China, the largest holder of US debt and the biggest consumer of gold in the world, has started openly talking about ending the dollar's reserve status. And while we don't know the total gold reserves of the Chinese government, there are signs that they are stockpiling.

Even US Treasury officials admit that the US will never sell its gold reserves to deal with debt obligations. One spokesperson said, "Selling gold would undercut confidence in the US both here and abroad, and would be destabilizing to the world financial system."

Time to Cash Out

So, who should investors believe about gold? Wall Street bankers who directly benefit from asset bubbles created by the Fed's inflationary stimulus?

No, it's time for individual investors to leave the table and redeem their chips. Just remember - the longer you wait to cash out of the US dollar, the less you're going to get for your winnings.

Peter Schiff is Chairman of Euro Pacific Precious Metals.

It's starting to feel like we are part of a giant poker game against the US government, whose hand is the true condition of the American economy. The government has become so good at bluffing that most people feel compelled to watch how the biggest players in the game react to determine their own investment strategy.

Unfortunately, this past month revealed that even pros like Goldman Sachs have no idea what sort of hand Washington is really hiding.

Goldman Bets Against Gold

A week into the government shutdown, Jeffrey Currie, head of commodities research at Goldman Sachs, declared that gold would be a "slam dunk sell" if Washington resolved the budget debate and raised the debt ceiling. The call was based on an underlying narrative that the US economy is experiencing a slow, but inevitable, recovery.

Taking this recovery as a foregone conclusion, conventional Wall Street analysts saw two clear choices for Washington. On the one hand, Congress could reach an agreement, raise the debt ceiling, and allow the recovery to continue. This would allegedly have been the final nail in the coffin of the safe-haven appeal of gold.

On the other hand, if no agreement were reached, the government would have been forced to default on its debt. This would have erased any signs of recovery and sent the economy spiraling back into a terrible recession - while boosting the gold price.

Goldman reasoned that Washington would never allow the latter to unfold and suggested investors prepare to short or sell gold.

While Washington did kick the debt can down the road as predicted, gold rallied 3% on the news - the complete opposite of expectations. That is, expectations outside of Euro Pacific.

Misreading the Signals

After seeing an investment theory crushed by reality, a rational investor would take a moment to reexamine his premises. In Goldman's case, this would mean second-guessing the conventional belief in an imminent or ongoing US economic recovery.

Yet, the day after Washington reached an agreement, Currie reaffirmed to Goldman's clients that his US economic outlook for 2014 is positive and that he believes gold faces "significant downside risks."

Currie must not have wanted to muddy his message by acknowledging that his original forecast was flat wrong. He did, however, hedge his statements by acknowledging that the Federal Reserve would likely hold off on tapering its stimulus until next year.

Major Wall Street investment houses have come to rely on the investing public's short-term memory to skate by on these bad calls. When the next forecast is issued, clients and subscribers quickly forget that Goldman was blindsided by the Fed's taper fakeout in September. [Read more about the taper fakeout in my previous Gold Letter.] That Currie accepted the government's new taper timeline within a month of being burned by the last shows how little stomach they have for sticking to the fundamentals - and how little accountability they face for getting it wrong.

Instead, major players like Goldman Sachs are betting their books on the government's fearless bluff. In the eyes of Wall Street, the economic indicators support this conclusion - inflation is subdued, GDP is growing!

The Bluff Exposed

I've been an outspoken critic of this official data for years. Over the course of my career, I have witnessed the government dramatically change the way it calculates inflation, GDP, and other statistics. While Washington's latest figures show a year-over-year CPI increase of just 1.2%, the private service ShadowStats, which recalculates the data along the lines that the government used to, finds that real consumer inflation is closer to 9%.

My guess is the true number lies somewhere in between, but that it would be much higher were the US not able to export much of its inflation abroad. The process works as follows: the Fed prints money (inflation) and uses it to buy Treasuries and mortgages. The government and banks, in turn, pass much of that money to consumers, who spend it on imported goods. The money then flows to foreign manufacturers of those products, who then sell it to their own central banks, who print their own currencies (inflation) to buy it. This money goes out to pay wages, rents, etc., which the recipients then spend on goods & services. Finally, the foreign central banks use the dollars they buy to purchase US Treasuries and mortgages, starting the cycle again.

It's a complicated relationship, but the end result is that inflation created in the US ultimately bids up consumer prices abroad and Treasury prices at home. In other words, our trading partners have to pay much more for goods & services while Americans get to borrow limitless money for next to nothing. The products our trading partners "sell" us increase the supply of goods available to American consumers while simultaneously decreasing the supply available to everyone else. That is what I mean by "exporting inflation," and the important thing to remember is that its result is to mask inflation at home and transfer wealth from emerging markets to the US.

The bluff gets worse. These understated CPI numbers distort real GDP, which would be lower if the true inflation rate were applied. The GDP calculations also include items like government expenditures, which are possible only because of money printing and not a result of any real economic production. Again, compare the official figure of 1-2% GDP growth in the second quarter of 2013 to ShadowStat's figure of negative 2%.

If investors can't bring themselves to question official data, there's another way to see through the government's bluff: look to foreign central banks, which are actively preparing for the day when the dollar is no longer the world's reserve currency.

The Bank of Italy recently affirmed that its gold reserves are essential to its economic independence, while the World Gold Council reported that this past year, European central banks held onto more of their gold reserves than ever before. China, the largest holder of US debt and the biggest consumer of gold in the world, has started openly talking about ending the dollar's reserve status. And while we don't know the total gold reserves of the Chinese government, there are signs that they are stockpiling.

Even US Treasury officials admit that the US will never sell its gold reserves to deal with debt obligations. One spokesperson said, "Selling gold would undercut confidence in the US both here and abroad, and would be destabilizing to the world financial system."

Time to Cash Out

So, who should investors believe about gold? Wall Street bankers who directly benefit from asset bubbles created by the Fed's inflationary stimulus?

No, it's time for individual investors to leave the table and redeem their chips. Just remember - the longer you wait to cash out of the US dollar, the less you're going to get for your winnings.

Peter Schiff is Chairman of Euro Pacific Precious Metals.

Volume Off the High- Nov. 7 Trading Day Edition

The number of names I have had to wade through has grown throughout the week, coming to head with yesterday's sell off. I would be surprised if we see another increase with today's trading. That said, a lot of names hit the list in yesterday's trading.

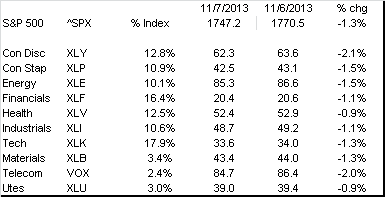

And Twitter Rings the Proverbial Bell- Price/Volume Heat Map for Nov. 7

Traders I have been listening to have been discussing the possibility that operators were holdings up the market ahead of the Twitter IPO, as to launch the company into a stronger market. Boy do they appear correct. Not only did we see a sell off, but the sell accelerated throughout the trading day yesterday, with the market essentially closing at its lows on higher than average volume levels. All in, the S&P 500 fell by about 130 basis points with all sectors experiencing losses.

As you might expect, the price/volume heat map is a virtual sea of red. Demand looks almost nonexistent. I will not go into any deep exploratory commentary here, but as I noted demand has been weak for days, despite continued market gains. Supply appears to have come back with a vengeance. We will have to see if it starts a new trend.

As you might expect, the price/volume heat map is a virtual sea of red. Demand looks almost nonexistent. I will not go into any deep exploratory commentary here, but as I noted demand has been weak for days, despite continued market gains. Supply appears to have come back with a vengeance. We will have to see if it starts a new trend.

Thursday, November 7, 2013

Gold's Direction Will Be Led by ECB Actions and Jobs Numbers- Hugg

Some short-term direction commentary.

Volume Off the High- Nov. 6 Trading Day Edition

The number of number of names coming off their highs with volume outnumbers new similar highs, and confirms my view that despite overall market gains, internal weakness remains.

Subscribe to:

Posts (Atom)