I was reading this article from the L.A. Times this morning providing details on Mitt Romney's trip to Appalachia and the Presidential candidate's accusation that Obama is "waging a war" on coal. If you have followed the coal stocks in 2012, you will have undoubtedly seen references to (be it on Street reports, stock message boards, or the media) Obama's war on coal, with many investors and coal stock followers attributing the massacre in the names to this attack.

Well, I am here to tell you that although the President is putting pressure on the coal industry, that this pressure is not the biggest contributor to the decline in coal stocks. You should remember that utility executives did not just wake up one day and decide to immediately throttle back and close coal-fired plants immediately because of federal mandates. Most, if not all, of announced coal-fired plant closures have specific time-tables attributable to them, making the issue manageable by the coal producers. It is not like plant closures happened overnight and without warning.

So what is the real culprit? The real "war" waged on the industry has been from a combination of a slowing economy and mother nature. My analysis of historical coal demand indicates that economic growth and the weather have an equal pull on the amount coal tons demanded in any year, some years the economy has a greater affect while it is the weather in others. On average, the split is about 50/50. It is my opinion that the weather is primary culprit for the coal industry's current woes.

Here is the thesis in three graphs with comments

The first is the difference in coal inventories experienced in the winter months of 2011 and 2012 vs. the five year average. This clearly shows the problem the industry was and is facing, as high inventories have yet to be worked off.

Now this does not prove anything in of itself, but the below the graph is also telling. Natural gas storage levels also built in the same time period, as exemplified by the below graph. This highlights, in my opinion, that the warmer-than-usual temperatures reeked havoc on the demand for energy. Increasing natural gas storage levels also provided double-whammy for coal. As natural gas storage levels increased, the price of natural gas decreased. This occurred amongst an increasing supply environment, as shale gas producers continued to drill. As the price of natural gas dipped below $2.75 to $3 per Mbtu in the early part of 2012, the demand for coal eroded further, as fuel-switching accelerated. (Note- every utility has different specifics and economics, but fuel switching typically begins to take place around $3 per Mbtu and accelerates as the price of natural gas falls below the $2.50 to $2.75 range.) The increase in natural gas storage levels began when the price of the commodity hovered in the mid-$3 range, and the increase in inventories could not have come at a worse time for coal producers.

A great deal of this inventory build was due to the warmer-than-average temperatures last winter, as heating-degree days was more than 14% below the 5-year average. Of course, the question is how much is due to weather and much was due to coal-plat retirements.

The above chart can help us derive that answer. The EIA is reporting that announced and planned coal-fired power plant retirements totaled about 2.5 gigawatts in 2011 and is estimated to be just below 9 gigawatts in 2012. Using industry sources, including presentations from Arch Coal and Peabody Energy, I estimate that these coal plant retirements would amount to about 38 million tons of lost coal demand. This compares to the net demand drop of about 60 million tons of coal, versus the five-year average, in the winter of 2011/2012. A quick comparison of these figures suggests that more than half of the demand drop could be due to plant closures, however there are caveats to this comparison. First, these retirements figures do not account for newly constructed or under construction coal-fired plants in either 2011 and 2012, estimated to be about 3 gigawatts of new coal-fired generating capacity, or a about a quarter of the completed/expected retirements. Nor is the tonnage comparison apples-to-apples on a time frame basis. that comparison would assume all the coal-plant retirements in 2011 and 2012 occurred between October 2011 and February 2012. If I had to guess, I would estimate that 15% to 35% of the decline in coal demand is due to coal-plant retirements. The remainder has been due to poor weather conditions- for coal companies anyway- in the winter of 2011/2012, the subsequent work down of high inventories levels, fuel switching at utilities as the price of natural gas swung to multi-year lows, and a slowing global economy.

Although the retirement plans will dent coal demand to some degree, most of the industries woes appear to be coming from other factors, factors that are not permanent. You should also remember that demand for coal worldwide will continue to grow, noting that many developing countries are structurally deficit in their own coal supplies, be it due to low available or poor quality supplies. This last point is key. World-wide higher quality supplies of coal are diminishing and many of the high quality coal mines are nearing the end of their useful lives. In my opinion, increased demand and diminishing supplies will support long-term prices.

Well, I am here to tell you that although the President is putting pressure on the coal industry, that this pressure is not the biggest contributor to the decline in coal stocks. You should remember that utility executives did not just wake up one day and decide to immediately throttle back and close coal-fired plants immediately because of federal mandates. Most, if not all, of announced coal-fired plant closures have specific time-tables attributable to them, making the issue manageable by the coal producers. It is not like plant closures happened overnight and without warning.

So what is the real culprit? The real "war" waged on the industry has been from a combination of a slowing economy and mother nature. My analysis of historical coal demand indicates that economic growth and the weather have an equal pull on the amount coal tons demanded in any year, some years the economy has a greater affect while it is the weather in others. On average, the split is about 50/50. It is my opinion that the weather is primary culprit for the coal industry's current woes.

Here is the thesis in three graphs with comments

The first is the difference in coal inventories experienced in the winter months of 2011 and 2012 vs. the five year average. This clearly shows the problem the industry was and is facing, as high inventories have yet to be worked off.

Now this does not prove anything in of itself, but the below the graph is also telling. Natural gas storage levels also built in the same time period, as exemplified by the below graph. This highlights, in my opinion, that the warmer-than-usual temperatures reeked havoc on the demand for energy. Increasing natural gas storage levels also provided double-whammy for coal. As natural gas storage levels increased, the price of natural gas decreased. This occurred amongst an increasing supply environment, as shale gas producers continued to drill. As the price of natural gas dipped below $2.75 to $3 per Mbtu in the early part of 2012, the demand for coal eroded further, as fuel-switching accelerated. (Note- every utility has different specifics and economics, but fuel switching typically begins to take place around $3 per Mbtu and accelerates as the price of natural gas falls below the $2.50 to $2.75 range.) The increase in natural gas storage levels began when the price of the commodity hovered in the mid-$3 range, and the increase in inventories could not have come at a worse time for coal producers.

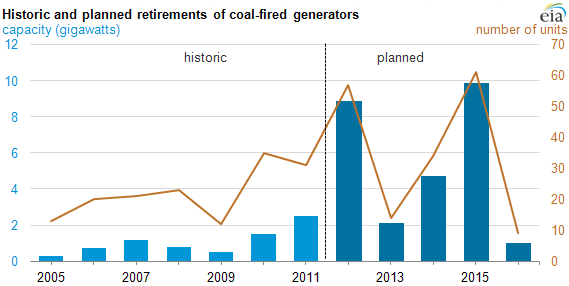

A great deal of this inventory build was due to the warmer-than-average temperatures last winter, as heating-degree days was more than 14% below the 5-year average. Of course, the question is how much is due to weather and much was due to coal-plat retirements.

The above chart can help us derive that answer. The EIA is reporting that announced and planned coal-fired power plant retirements totaled about 2.5 gigawatts in 2011 and is estimated to be just below 9 gigawatts in 2012. Using industry sources, including presentations from Arch Coal and Peabody Energy, I estimate that these coal plant retirements would amount to about 38 million tons of lost coal demand. This compares to the net demand drop of about 60 million tons of coal, versus the five-year average, in the winter of 2011/2012. A quick comparison of these figures suggests that more than half of the demand drop could be due to plant closures, however there are caveats to this comparison. First, these retirements figures do not account for newly constructed or under construction coal-fired plants in either 2011 and 2012, estimated to be about 3 gigawatts of new coal-fired generating capacity, or a about a quarter of the completed/expected retirements. Nor is the tonnage comparison apples-to-apples on a time frame basis. that comparison would assume all the coal-plant retirements in 2011 and 2012 occurred between October 2011 and February 2012. If I had to guess, I would estimate that 15% to 35% of the decline in coal demand is due to coal-plant retirements. The remainder has been due to poor weather conditions- for coal companies anyway- in the winter of 2011/2012, the subsequent work down of high inventories levels, fuel switching at utilities as the price of natural gas swung to multi-year lows, and a slowing global economy.

Although the retirement plans will dent coal demand to some degree, most of the industries woes appear to be coming from other factors, factors that are not permanent. You should also remember that demand for coal worldwide will continue to grow, noting that many developing countries are structurally deficit in their own coal supplies, be it due to low available or poor quality supplies. This last point is key. World-wide higher quality supplies of coal are diminishing and many of the high quality coal mines are nearing the end of their useful lives. In my opinion, increased demand and diminishing supplies will support long-term prices.

No comments:

Post a Comment